estimate

Estimate posterior distribution of Bayesian state-space model parameters

Since R2022a

Syntax

Description

PosteriorMdl = estimate(PriorMdl,Y,params0)PosteriorMdl from

combining the Bayesian state-space model prior distribution and likelihood

PriorMdl with the response data Y. The input

argument params0 is the vector of initial values for the unknown

state-space model parameters Θ in PriorMdl.

PosteriorMdl = estimate(PriorMdl,Y,params0,Name=Value)estimate(Mdl,Y,params0,NumDraws=1e6,Thin=3,DoF=10) uses the

multivariate t10 distribution for the

Metropolis-Hastings [1][2] proposal, draws 3e6

random vectors of parameters, and thins the sample to reduce serial correlation by

discarding every 2 draws until it retains 1e6 draws.

[

additionally returns the following quantities using any of the input-argument combinations

in the previous syntaxes:PosteriorMdl,estParams,EstParamCov,Summary]

= estimate(___)

estParams— A vector containing the estimated parameters Θ.EstParamCov— The estimated variance-covariance matrix of the estimated parameters Θ.Summary— Estimation summary of the posterior distribution of parameters Θ. If the distribution of the state disturbances or observation innovations is non-Gaussian,Summaryalso includes the estimation summary of the final state values, and any estimated disturbance or innovation distribution hyperparameters.

Examples

Simulate observed responses from a known state-space model, then treat the model as Bayesian and estimate the posterior distribution of the parameters by treating the state-space model parameters as unknown.

Suppose the following state-space model is a data-generating process (DGP).

Create a standard state-space model object ssm that represents the DGP.

trueTheta = [0.5; -0.75; 1; 0.5]; A = [trueTheta(1) 0; 0 trueTheta(2)]; B = [trueTheta(3) 0; 0 trueTheta(4)]; C = [1 1]; DGP = ssm(A,B,C);

Simulate a response path from the DGP.

rng(1); % For reproducibility

y = simulate(DGP,200);Suppose the structure of the DGP is known, but the state parameters trueTheta are unknown, explicitly

Consider a Bayesian state-space model representing the model with unknown parameters. Arbitrarily assume that the prior distribution of , , , and are independent Gaussian random variables with mean 0.5 and variance 1.

The Local Functions section contains two functions required to specify the Bayesian state-space model. You can use the functions only within this script.

The paramMap function accepts a vector of the unknown state-space model parameters and returns all the following quantities:

A= .B= .C= .D= 0.Mean0andCov0are empty arrays[], which specify the defaults.StateType= , indicating that each state is stationary.

The paramDistribution function accepts the same vector of unknown parameters as does paramMap, but it returns the log prior density of the parameters at their current values. Specify that parameter values outside the parameter space have log prior density of -Inf.

Create the Bayesian state-space model by passing function handles directly to paramMap and paramDistribution to bssm.

PriorMdl = bssm(@paramMap,@priorDistribution)

PriorMdl =

Mapping that defines a state-space model:

@paramMap

Log density of parameter prior distribution:

@priorDistribution

PriorMdl is a bssm object representing the Bayesian state-space model with unknown parameters.

Estimate the posterior distribution using default options of estimate. Specify a random set of positive values in [0,1] to initialize the MCMC algorithm.

numParams = 4; theta0 = rand(numParams,1); PosteriorMdl = estimate(PriorMdl,y,theta0);

Local minimum found.

Optimization completed because the size of the gradient is less than

the value of the optimality tolerance.

<stopping criteria details>

Optimization and Tuning

| Params0 Optimized ProposalStd

----------------------------------------

c(1) | 0.6968 0.4459 0.0798

c(2) | 0.7662 -0.8781 0.0483

c(3) | 0.3425 0.9633 0.0694

c(4) | 0.8459 0.3978 0.0726

Posterior Distributions

| Mean Std Quantile05 Quantile95

------------------------------------------------

c(1) | 0.4491 0.0905 0.3031 0.6164

c(2) | -0.8577 0.0606 -0.9400 -0.7365

c(3) | 0.9589 0.0695 0.8458 1.0699

c(4) | 0.4316 0.0893 0.3045 0.6023

Proposal acceptance rate = 40.10%

PosteriorMdl.ParamMap

ans = function_handle with value:

@paramMap

ThetaPostDraws = PosteriorMdl.ParamDistribution; [numParams,numDraws] = size(ThetaPostDraws)

numParams = 4

numDraws = 1000

estimate finds an optimal proposal distribution for the Metropolis-Hastings sampler by using the tune function. Therefore, by default, estimate prints convergence information from tune. Also, estimate displays a summary of the posterior distribution of the parameters. The true values of the parameters are close to their corresponding posterior means; all are within their corresponding 95% credible intervals.

PosteriorMdl is a bssm object representing the posterior distribution.

PosteriorMdl.ParamMapis the function handle to the function representing the state-space model structure; it is the same function asPrioirMdl.ParamMap.ThetaPostDrawsis a 4-by-1000 matrix of draws from the posterior distribution. By default,estimatetreats the first 100 draws as a burn-in sample and removes them from the matrix.

To diagnose the Markov chain induced by the Metropolis-Hastings sampler, create trace plots of the posterior parameter draws.

paramNames = ["\phi_1" "\phi_2" "\sigma_1" "\sigma_2"]; figure h = tiledlayout(4,1); for j = 1:numParams nexttile plot(ThetaPostDraws(j,:)) hold on yline(trueTheta(j)) ylabel(paramNames(j)) end title(h,"Posterior Trace Plots")

The sampler eventually settles at near the true values of the parameters. In this case, the sample shows serial correlation and transient behavior. You can remedy serial correlation in the sample by adjusting the Thin name-value argument, and you can remedy transient effects by increasing the burn-in period using the BurnIn name-value argument.

Local Functions

This example uses the following functions. paramMap is the parameter-to-matrix mapping function and priorDistribution is the log prior distribution of the parameters.

function [A,B,C,D,Mean0,Cov0,StateType] = paramMap(theta) A = [theta(1) 0; 0 theta(2)]; B = [theta(3) 0; 0 theta(4)]; C = [1 1]; D = 0; Mean0 = []; % MATLAB uses default initial state mean Cov0 = []; % MATLAB uses initial state covariances StateType = [0; 0]; % Two stationary states end function logprior = priorDistribution(theta) paramconstraints = [(abs(theta(1)) >= 1) (abs(theta(2)) >= 1) ... (theta(3) < 0) (theta(4) < 0)]; if(sum(paramconstraints)) logprior = -Inf; else mu0 = 0.5*ones(numel(theta),1); sigma0 = 1; p = normpdf(theta,mu0,sigma0); logprior = sum(log(p)); end end

Consider the model in the example Estimate Posterior Distribution of Time-Invariant Model. Improve the Markov chain convergence by adjusting sampler options.

Create a standard state-space model object ssm that represents the DGP, and then simulate a response path.

trueTheta = [0.5; -0.75; 1; 0.5];

A = [trueTheta(1) 0; 0 trueTheta(2)];

B = [trueTheta(3) 0; 0 trueTheta(4)];

C = [1 1];

DGP = ssm(A,B,C);

rng(1); % For reproducibility

y = simulate(DGP,200);Create a Bayesian state-space model template for estimation by passing function handles directly to paramMap and paramDistribution to bssm (the functions are in Local Functions).

Mdl = bssm(@paramMap,@priorDistribution);

Estimate the posterior distribution. Specify the simulated response path as observed responses, specify a random set of positive values in [0,1] to initialize the MCMC algorithm, and shut off all optimization displays. The plots in Estimate Posterior Distribution of Time-Invariant Model suggest that the Markov chain settles after 500 draws. Therefore, specify a burn-in period of 500 (BurnIn=500). Specify thinning the sample by keeping the first draw of each set of 30 successive draws (Thin=30). Retain 2000 random parameter vectors (NumDraws=2000).

numParams = 4; theta0 = rand(numParams,1); options = optimoptions("fminunc",Display="off"); PosteriorMdl = estimate(Mdl,y,theta0,Options=options, ... NumDraws=2000,BurnIn=500,Thin=30);

Optimization and Tuning

| Params0 Optimized ProposalStd

----------------------------------------

c(1) | 0.6968 0.4459 0.0798

c(2) | 0.7662 -0.8781 0.0483

c(3) | 0.3425 0.9633 0.0694

c(4) | 0.8459 0.3978 0.0726

Posterior Distributions

| Mean Std Quantile05 Quantile95

------------------------------------------------

c(1) | 0.4495 0.0822 0.3135 0.5858

c(2) | -0.8561 0.0587 -0.9363 -0.7468

c(3) | 0.9645 0.0744 0.8448 1.0863

c(4) | 0.4333 0.0860 0.3086 0.5889

Proposal acceptance rate = 38.85%

ThetaPostDraws = PosteriorMdl.ParamDistribution;

Plot trace plots and correlograms of the parameters.

paramNames = ["\phi_1" "\phi_2" "\sigma_1" "\sigma_2"]; figure h = tiledlayout(4,1); for j = 1:numParams nexttile plot(ThetaPostDraws(j,:)) hold on yline(trueTheta(j)) ylabel(paramNames(j)) end title(h,"Posterior Trace Plots")

figure h = tiledlayout(4,1); for j = 1:numParams nexttile autocorr(ThetaPostDraws(j,:)); ylabel(paramNames(j)); title([]); end title(h,"Posterior Sample Correlograms")

The sampler quickly settles near the true values of the parameters. The sample shows little serial correlation and no transient behavior.

Local Functions

This example uses the following functions. paramMap is the parameter-to-matrix mapping function and priorDistribution is the log prior distribution of the parameters.

function [A,B,C,D,Mean0,Cov0,StateType] = paramMap(theta) A = [theta(1) 0; 0 theta(2)]; B = [theta(3) 0; 0 theta(4)]; C = [1 1]; D = 0; Mean0 = []; % MATLAB uses default initial state mean Cov0 = []; % MATLAB uses initial state covariances StateType = [0; 0]; % Two stationary states end function logprior = priorDistribution(theta) paramconstraints = [(abs(theta(1)) >= 1) (abs(theta(2)) >= 1) ... (theta(3) < 0) (theta(4) < 0)]; if(sum(paramconstraints)) logprior = -Inf; else mu0 = 0.5*ones(numel(theta),1); sigma0 = 1; p = normpdf(theta,mu0,sigma0); logprior = sum(log(p)); end end

Simulate observed responses from a DGP, then treat the model as Bayesian and estimate the posterior distribution of the model parameters and the degrees of freedom of multivariate -distributed state disturbances.

Consider the following DGP.

The true value of the state-space parameter set .

The state disturbances and are jointly a multivariate Student's random series with degrees of freedom.

Create a vector autoregression (VAR) model that represents the state equation of the DGP.

trueTheta = [0.5; -0.75; 1; 0.5];

trueDoF = 5;

phi = [trueTheta(1) 0; 0 trueTheta(2)];

Sigma = [trueTheta(3)^2 0; 0 trueTheta(4)^2];

DGP = varm(AR={phi},Covariance=Sigma,Constant=[0; 0]);Filter a random 2-D multivariate central series of length 500 through the VAR model to obtain state values. Set the degrees of freedom to 5.

rng(10) % For reproducibility

T = 500;

trueU = mvtrnd(eye(DGP.NumSeries),trueDoF,T);

X = filter(DGP,trueU);Obtain a series of observations from the DGP by the linear combination .

C = [1 3]; y = X*C';

Consider a Bayesian state-space model representing the model with parameters and treated as unknown. Arbitrarily assume that the prior distribution of the parameters in are independent Gaussian random variables with mean 0.5 and variance 1. Assume that the prior on the degrees of freedom is flat. The functions in Local Functions specify the state-space structure and prior distributions.

Create the Bayesian state-space model by passing function handles to the paramMap and priorDistribution functions to bssm. Specify that the state disturbance distribution is multivariate Student's with unknown degrees of freedom.

PriorMdl = bssm(@paramMap,@priorDistribution,StateDistribution="t");PriorMdl is a bssm object representing the Bayesian state-space model with unknown parameters.

Estimate the posterior distribution by using estimate. Specify a random set of positive values in [0,1] to initialize the MCMC algorithm. Set the burn-in period of the MCMC algorithm to 1000 draws, thin the entire MCMC sample by retaining every third draw, and set the proposal scale matrix proportionality constant to 0.25 to increase the proposal acceptance rate.

numParamsTheta = 4; theta0 = rand(numParamsTheta,1); PosteriorMdl = estimate(PriorMdl,y,theta0,Thin=3,BurnIn=1000,Proportion=0.25);

Local minimum found.

Optimization completed because the size of the gradient is less than

the value of the optimality tolerance.

<stopping criteria details>

Optimization and Tuning

| Params0 Optimized ProposalStd

----------------------------------------

c(1) | 0.9219 0.3622 0.1151

c(2) | 0.9475 -0.7530 0.0454

c(3) | 0.2299 1.3465 0.1917

c(4) | 0.6759 0.5891 0.0545

Posterior Distributions

| Mean Std Quantile05 Quantile95

----------------------------------------------------

c(1) | 0.4516 0.1036 0.2641 0.5972

c(2) | -0.7459 0.0376 -0.8085 -0.6863

c(3) | 0.9816 0.1526 0.7430 1.2494

c(4) | 0.4843 0.0402 0.4234 0.5520

x(1) | -1.1901 0.9271 -2.7359 0.2539

x(2) | 0.2133 0.3090 -0.2680 0.7286

StateDoF | 5.3980 0.7931 4.1574 6.7111

Proposal acceptance rate = 51.10%

ThetaPostDraws = PosteriorMdl.ParamDistribution; [numParams,numDraws] = size(ThetaPostDraws)

numParams = 4

numDraws = 1000

estimate displays a summary of the posterior distribution of the parameters (c(1) through c(4)), the final values of the two states (x(1) and x(2)), and (StateDoF). The true values of the parameters are close to their corresponding posterior means; all are within their corresponding 95% credible intervals.

PosteriorMdl is a bssm object representing the posterior distribution.

PosteriorMdl.ParamMapis the function handle to the function representing the state-space model structure. It is the same function asPrioirMdl.ParamMap.ThetaPostDrawsis a 4-by-1000 matrix of draws from the posterior distribution of .

To diagnose the Markov chain induced by the Metropolis-Hastings sampler, create trace plots of the posterior parameter draws of .

paramNames = ["\phi_1" "\phi_2" "\sigma_1" "\sigma_2"]; figure h = tiledlayout(4,1); for j = 1:numParams nexttile plot(ThetaPostDraws(j,:)) hold on yline(trueTheta(j)) ylabel(paramNames(j)) end title(h,"Posterior Trace Plots")

The sample shows some serial correlation. You can increase Thin to remedy this behavior.

Local Functions

This example uses the following functions. paramMap is the parameter-to-matrix mapping function and priorDistribution is the log prior distribution of the parameters.

function [A,B,C,D,Mean0,Cov0,StateType] = paramMap(theta) A = [theta(1) 0; 0 theta(2)]; B = [theta(3) 0; 0 theta(4)]; C = [1 3]; D = 0; Mean0 = []; % MATLAB uses default initial state mean Cov0 = []; % MATLAB uses initial state covariances StateType = [0; 0]; % Two stationary states end function logprior = priorDistribution(theta) paramconstraints = [(abs(theta(1)) >= 1) (abs(theta(2)) >= 1) ... (theta(3) < 0) (theta(4) < 0)]; if(sum(paramconstraints)) logprior = -Inf; else mu0 = 0.5*ones(numel(theta),1); sigma0 = 1; p = normpdf(theta,mu0,sigma0); logprior = sum(log(p)); end end

Consider the following time-varying, state-space model for a DGP:

From periods 1 through 250, the state equation includes stationary AR(2) and MA(1) models, respectively, and the observation model is the weighted sum of the two states.

From periods 251 through 500, the state model includes only the first AR(2) model.

and is the identity matrix.

Symbolically, the DGP is

where:

The AR(2) parameters and .

The MA(1) parameter .

The observation equation parameters and .

Write a function that specifies how the parameters theta and sample size T map to the state-space model matrices, the initial state moments, and the state types. Save this code as a file named timeVariantParamMapBayes.m on your MATLAB® path. Alternatively, open the example to access the function.

type timeVariantParamMapBayes.m% Copyright 2022 The MathWorks, Inc.

function [A,B,C,D,Mean0,Cov0,StateType] = timeVariantParamMapBayes(theta,T)

% Time-variant, Bayesian state-space model parameter mapping function

% example. This function maps the vector params to the state-space matrices

% (A, B, C, and D), the initial state value and the initial state variance

% (Mean0 and Cov0), and the type of state (StateType). From periods 1

% through T/2, the state model is a stationary AR(2) and an MA(1) model,

% and the observation model is the weighted sum of the two states. From

% periods T/2 + 1 through T, the state model is the AR(2) model only. The

% log prior distribution enforces parameter constraints (see

% flatPriorBSSM.m).

T1 = floor(T/2);

T2 = T - T1 - 1;

A1 = {[theta(1) theta(2) 0 0; 1 0 0 0; 0 0 0 theta(4); 0 0 0 0]};

B1 = {[theta(3) 0; 0 0; 0 1; 0 1]};

C1 = {theta(5)*[1 0 1 0]};

D1 = {theta(6)};

Mean0 = [0.5 0.5 0 0];

Cov0 = eye(4);

StateType = [0 0 0 0];

A2 = {[theta(1) theta(2) 0 0; 1 0 0 0]};

B2 = {[theta(3); 0]};

A3 = {[theta(1) theta(2); 1 0]};

B3 = {[theta(3); 0]};

C3 = {theta(7)*[1 0]};

D3 = {theta(8)};

A = [repmat(A1,T1,1); A2; repmat(A3,T2,1)];

B = [repmat(B1,T1,1); B2; repmat(B3,T2,1)];

C = [repmat(C1,T1,1); repmat(C3,T2+1,1)];

D = [repmat(D1,T1,1); repmat(D3,T2+1,1)];

end

Simulate a response path of length 500 from the model.

params = [0.5; -0.2; 0.4; 0.3; 2; 0.1; 3; 0.2]; numParams = numel(params); numObs = 500; [A,B,C,D,mean0,Cov0,stateType] = timeVariantParamMapBayes(params,numObs); DGP = ssm(A,B,C,D,Mean0=mean0,Cov0=Cov0,StateType=stateType); rng(1) % For reproducibility y = simulate(DGP,numObs); plot(y) ylabel("y")

Write a function that specifies a flat prior distribution on the state-space model parameters theta. The function returns the scalar log prior for an input set of parameters. Save this code as a file named flatPriorBSSM.m on your MATLAB® path. Alternatively, open the example to access the function.

type flatPriorBSSM.m% Copyright 2022 The MathWorks, Inc.

function logprior = flatPriorBSSM(theta)

% flatPriorBSSM computes the log of the flat prior density for the eight

% variables in theta (see timeVariantParamMapBayes.m). Log probabilities

% for parameters outside the parameter space are -Inf.

% theta(1) and theta(2) are lag 1 and lag 2 terms in a stationary AR(2)

% model. The eigenvalues of the AR(1) representation need to be within

% the unit circle.

evalsAR2 = eig([theta(1) theta(2); 1 0]);

evalsOutUC = sum(abs(evalsAR2) >= 1) > 0;

% Standard deviations of disturbances and errors (theta(3), theta(6),

% and theta(8)) need to be positive.

nonnegsig1 = theta(3) <= 0;

nonnegsig2 = theta(6) <= 0;

nonnegsig3 = theta(8) <= 0;

paramconstraints = [evalsOutUC nonnegsig1 ...

nonnegsig2 nonnegsig3];

if sum(paramconstraints) > 0

logprior = -Inf;

else

logprior = 0; % Prior density is proportional to 1 for all values

% in the parameter space.

end

end

Create a time-varying, Bayesian state-space model that uses the structure of the DGP.

Mdl = bssm(@(params)timeVariantParamMapBayes(params,numObs),@flatPriorBSSM);

Estimate the posterior distribution. Initialize the parameter values for the MCMC algorithm with a random set of positive values in [0,0.5]. Set the proposal distribution to multivariate . Set the proportionality constant of the proposal distribution scale matrix to 0.005. Shut off all displays. Return the posterior distribution, estimated posterior means of the parameters, estimated covariance matrix of the estimated parameters, and an estimation summary.

params0 = 0.5*rand(numParams,1); options = optimoptions("fminunc",Display="off"); [PostParams,estParams,EstParamCov,Summary] = estimate(Mdl,y,params0, ... DoF=25,Proportion=0.005,Display=false,Options=options); [params estParams]

ans = 8×2

0.5000 0.5316

-0.2000 -0.2426

0.4000 1.0264

0.3000 0.8591

2.0000 0.9776

0.1000 1.3845

3.0000 1.2031

0.2000 0.1419

EstParamCov

EstParamCov = 8×8

0.0020 -0.0011 0.0010 0.0219 -0.0071 0.0025 -0.0021 0.0028

-0.0011 0.0012 -0.0009 -0.0127 0.0044 -0.0011 0.0014 -0.0012

0.0010 -0.0009 0.0250 0.0138 -0.0140 0.0006 -0.0285 0.0011

0.0219 -0.0127 0.0138 0.3248 -0.1045 0.0364 -0.0290 0.0282

-0.0071 0.0044 -0.0140 -0.1045 0.0386 -0.0136 0.0199 -0.0079

0.0025 -0.0011 0.0006 0.0364 -0.0136 0.0138 -0.0018 0.0027

-0.0021 0.0014 -0.0285 -0.0290 0.0199 -0.0018 0.0333 -0.0026

0.0028 -0.0012 0.0011 0.0282 -0.0079 0.0027 -0.0026 0.0113

Summary

Summary=8×4 table

Mean Std Quantile05 Quantile95

________ ________ __________ __________

0.53161 0.045129 0.46479 0.60354

-0.24257 0.035128 -0.31361 -0.20298

1.0264 0.15825 0.76022 1.3017

0.85906 0.56993 0.10817 1.7896

0.9776 0.1964 0.68948 1.2572

1.3845 0.11755 1.1687 1.5508

1.2031 0.18256 0.90772 1.5014

0.14193 0.10637 0.012756 0.3645

The sampler has some trouble estimating several parameters. You can improve posterior estimation by diagnosing the properties of the Metropolis-Hasting sample.

When you work with a state-space model that contains a deflated response variable, you must have data for the predictors.

Consider a regression of the US unemployment rate onto and real gross national product (RGNP) rate, and suppose the resulting innovations are an ARMA(1,1) process. The state-space form of the relationship is

where:

is the ARMA process.

is a dummy state for the MA(1) effect.

is the observed unemployment rate deflated by a constant and the RGNP rate ().

is an iid Gaussian series with mean 0 and standard deviation 1.

Load the Nelson-Plosser data set, which contains a table DataTable that has the unemployment rate and RGNP series, among other series.

load Data_NelsonPlosserCreate a variable in DataTable that represents the returns of the raw RGNP series. Because price-to-returns conversion reduces the sample size by one, prepad the series with NaN.

DataTable.RGNPRate = [NaN; price2ret(DataTable.GNPR)]; T = height(DataTable);

Create variables for the regression. Represent the unemployment rate as the observation series and the constant and RGNP rate series as the deflation data .

Z = [ones(T,1) DataTable.RGNPRate]; y = DataTable.UR;

Write a function that specifies how the parameters theta, response series y, and deflation data Z map to the state-space model matrices, the initial state moments, and the state types. Save this code as a file named armaDeflateYBayes.m on your MATLAB® path. Alternatively, open the example to access the function.

type armaDeflateYBayes.m% Copyright 2022 The MathWorks, Inc.

function [A,B,C,D,Mean0,Cov0,StateType,DeflatedY] = armaDeflateYBayes(theta,y,Z)

% Time-invariant, Bayesian state-space model parameter mapping function

% example. This function maps the vector parameters to the state-space

% matrices (A, B, C, and D), the default initial state value and the

% default initial state variance (Mean0 and Cov0), the type of state

% (StateType), and the deflated observations (DeflatedY). The log prior

% distribution enforces parameter constraints (see flatPriorDeflateY.m).

A = [theta(1) theta(2); 0 0];

B = [theta(3); 1];

C = [1 0];

D = 0;

Mean0 = [];

Cov0 = [];

StateType = [0 0];

DeflatedY = y - Z*[theta(4); theta(5)];

end

Write a function that specifies a flat prior distribution on the state-space model parameters theta. The function returns the scalar log prior for an input set of parameters. Save this code as a file named flatPriorDeflateY.m on your MATLAB® path. Alternatively, open the example to access the function.

type flatPriorDeflateY.m% Copyright 2022 The MathWorks, Inc.

function logprior = flatPriorDeflateY(theta)

% flatPriorDeflateY computes the log of the flat prior density for the five

% variables in theta (see armaDeflateYBayes.m). Log probabilities

% for parameters outside the parameter space are -Inf.

% theta(1) and theta(2) are the AR and MA terms in a stationary

% ARMA(1,1) model. The AR term must be within the unit circle.

AROutUC = abs(theta(1)) >= 1;

% The standard deviation of innovations (theta(3)) must be positive.

nonnegsig1 = theta(3) <= 0;

paramconstraints = [AROutUC nonnegsig1];

if sum(paramconstraints) > 0

logprior = -Inf;

else

logprior = 0; % Prior density is proportional to 1 for all values

% in the parameter space.

end

end

Create a bssm object representing the Bayesian state-space model. Specify the parameter-to-matrix mapping function as a handle to a function solely of the parameters.

numParams = 5; Mdl = bssm(@(params)armaDeflateYBayes(params,y,Z),@flatPriorDeflateY)

Mdl =

Mapping that defines a state-space model:

@(params)armaDeflateYBayes(params,y,Z)

Log density of parameter prior distribution:

@flatPriorDeflateY

Estimate the posterior distribution. Initialize the MCMC algorithm with a random set of positive values in [0,0.5]. Set the proportionality constant to 0.01. Set a burn-in period of 2000 draws, set a thinning factor of 50, and specify retaining 1000 draws. Return an estimation summary table.

rng(1) % For reproducibility params0 = 0.5*rand(numParams,1); options = optimoptions("fminunc",Display="off"); [~,~,~,Summary] = estimate(Mdl,y,params0,Proportion=0.01, ... BurnIn=2000,NumDraws=1000,Thin=50,Options=options,Display=false); Summary

Summary=5×4 table

Mean Std Quantile05 Quantile95

_______ ________ __________ __________

0.83814 0.072544 0.71734 0.9582

1.8193 0.22216 1.4235 2.1651

1.6905 0.29097 1.2282 2.1925

7.22 3.5132 2.2481 12.585

-15.099 1.6741 -17.582 -12.361

Input Arguments

Name-Value Arguments

Output Arguments

Algorithms

The Kalman filter accommodates missing data by not updating filtered state estimates corresponding to missing observations. In other words, suppose there is a missing observation at period t. Then, the state forecast for period t based on the previous t – 1 observations and filtered state for period t are equivalent.

estimateuses thetunefunction to create the proposal distribution for the Metropolis-Hastings sampler. You can tune the sampler by using the proposal tuning options.When

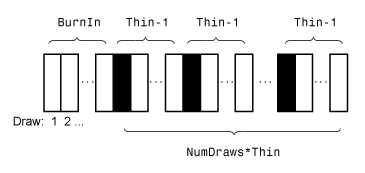

estimatetunes the proposal distribution, the optimizer thatestimateuses to search for the posterior mode before computing the Hessian matrix depends on your specifications.This figure shows how

estimatereduces the sample by using the values ofNumDraws,Thin, andBurnIn. Rectangles represent successive draws from the distribution.estimateremoves the white rectangles from the sample. The remainingNumDrawsblack rectangles compose the sample.

References

Version History

Introduced in R2022a