ret2price

Convert returns to prices

Syntax

Description

PriceTbl = ret2price(ReturnTbl)DataVariables

name-value argument. (since R2022a)

[___] = ret2price(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)ret2price returns the output argument combination for the

corresponding input arguments. For example,

ret2price(Tbl,Method="periodic",DataVariables=1:5) computes prices from

the simple periodic returns in the first five variables in the input table

Tbl. (since R2022a)

Examples

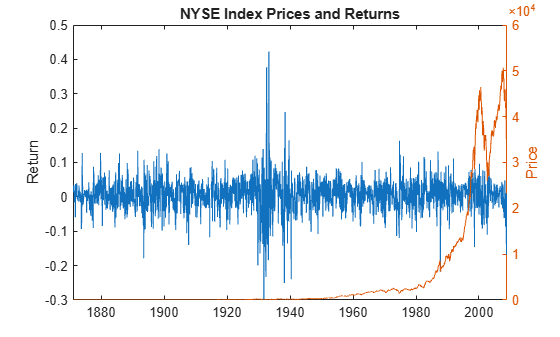

Load the Schwert Stock data set Data_SchwertStock.mat, which contains monthly returns of the NYSE index from 1871 through 2008 DataTableMth.Return, among other variables (enter Description for more details).

load Data_SchwertStock

returns = DataTableMth.Return;

numObs = numel(returns)numObs = 1656

dates = datetime(datesMth,ConvertFrom="datenum");Set missing (NaN) returns to 0.

returns(isnan(returns)) = 0;

Convert the monthly NYSE returns to prices.

prices = ret2price(returns);

prices is a 1657-by-1 vector of monthly NYSE prices from the continuously compounded returns. ret2price sets the starting price to 1 by default; specify the StartPrice name-value argument to set an appropriate starting price.

r10 = returns(9)

r10 = 0.0114

p9_10 = [prices(9) prices(10)]

p9_10 = 1×2

1.1274 1.1403

returns(10) = 0.0114 is the monthly return of the prices in the interval [1.1274, 1.1403].

plot(dates,DataTableMth.Return) ylabel("Return") yyaxis right plot([dates(1) - month(1); dates],prices) ylabel("Price") title("NYSE Index Prices and Returns")

Since R2022a

Compute price series from return series, which are variables in a table. This example also shows how to convert prices in a timetable.

Load and Preprocess Data

Load the Schwert Stock data set Data_SchwertStock.mat, which contains monthly returns of several series in the table DataTableMth. Replace all missing values (NaN) with 0.

load Data_SchwertStock DTM = fillmissing(DataTableMth,"constant",0);

Convert Returns in Table to Prices

Convert all return series in the table to prices.

PriceTbl = ret2price(DTM); tail(PriceTbl)

Tick Interval Return DivYld CapGain CapGainA

____ ________ ______ ______ _______ ________

1649 1 46004 16.9 5.3445 5.4712

1650 1 42215 16.9 5.3445 5.4712

1651 1 41801 16.9 5.3445 5.4712

1652 1 42313 16.9 5.3445 5.4712

1653 1 38592 16.9 5.3445 5.4712

1654 1 32615 16.9 5.3445 5.4712

1655 1 30263 16.9 5.3445 5.4712

1656 1 30501 16.9 5.3445 5.4712

Because DTM is a table, PriceTbl is a table. PriceTbl contains the price series computed from the continuously compounded returns (variable names match the input variable names), observation times Tick, and time intervals Interval.

You can choose a subset of variables to convert to prices by using the DataVariables name-value argument.

Convert Returns in Timetable to Prices

Convert the table DTM to a timetable.

dates = datetime(datesMth,ConvertFrom="datenum");

TT = table2timetable(DTM,RowTimes=dates);

TT.Dates = [];When the input series is a timetable, ret2price requires a starting time, which is specified by the StartTime name-value argument.

Convert only the NYSE and capital gain returns to prices, and specify the following options:

The starting time is exactly one month before the first observed return.

The starting prices of the NYSE and capital gains returns are 100 and 10, respectively.

The returns are periodic.

startTime = TT.Time(1) - month(1); varnames = ["Return" "CapGain"]; startPrice = [100 10]; PriceTT = ret2price(TT,DataVariables=varnames,Method="periodic", ... StartTime=startTime,StartPrice=startPrice); head(PriceTT)

Time Interval Return CapGain

___________ ________ ______ _______

31-Dec-1870 NaN 100 10

01-Jan-1871 1 101.24 10.023

01-Feb-1871 31 164.61 14.374

01-Mar-1871 28 301.26 24.381

01-Apr-1871 31 619.29 46.79

01-May-1871 30 1148.5 79.862

01-Jun-1871 31 599.29 60.866

01-Jul-1871 30 443.99 27.923

Because TT is a timetable, PriceTT is a timetable. PriceTT contains only those requested price series. Because the input data is time aware, the time-related variables in PriceTT contain more information about the observation times than returned when the input data is a matrix or table. For example, rather than tick times, the output timetable contains observation dates for the prices and the interval is in days.

Since R2022a

Create two stock price series from continuously compounded returns that have the following characteristics:

Series 1 grows at a 10 percent rate at each observation time.

Series 2 changes at a random uniform rate in the interval [-0.1, 0.1] at each observation time.

Each series starts at price 100 and is 10 observations in length.

rng(1); % For reproducibility

numObs = 10;

p1 = 100;

r1 = 0.10;

r2 = [0; unifrnd(-0.10,0.10,numObs - 1,1)];

s1 = 100*exp(r1*(0:(numObs - 1))');

cr2 = cumsum(r2);

s2 = 100*exp(cr2);

S = [s1 s2];Convert each price series to a return series, and return the observation intervals.

[R,intervals] = price2ret(S);

Prepend the return series so that the input and output elements are of the same length and correspond.

[[NaN; intervals] S [[NaN NaN]; R] r2]

ans = 10×6

NaN 100.0000 100.0000 NaN NaN 0

1.0000 110.5171 98.3541 0.1000 -0.0166 -0.0166

1.0000 122.1403 102.7850 0.1000 0.0441 0.0441

1.0000 134.9859 93.0058 0.1000 -0.1000 -0.1000

1.0000 149.1825 89.4007 0.1000 -0.0395 -0.0395

1.0000 164.8721 83.3026 0.1000 -0.0706 -0.0706

1.0000 182.2119 76.7803 0.1000 -0.0815 -0.0815

1.0000 201.3753 72.1105 0.1000 -0.0627 -0.0627

1.0000 222.5541 69.9172 0.1000 -0.0309 -0.0309

1.0000 245.9603 68.4885 0.1000 -0.0206 -0.0206

price2ret returns rates matching the rates from the simulated series. price2ret assumes prices are recorded in a regular time base, therefore all durations between prices are 1.

Convert the prices to returns again, but associate the prices with years starting from August 1, 2010.

tau1 = datetime(2010,08,01); dates = tau1 + years((0:(numObs-1))'); [Ry,intervalsy] = price2ret(S,Ticks=dates); [[NaN; intervalsy] S [[NaN NaN]; Ry] r2]

ans = 10×6

NaN 100.0000 100.0000 NaN NaN 0

365.2425 110.5171 98.3541 0.0003 -0.0000 -0.0166

365.2425 122.1403 102.7850 0.0003 0.0001 0.0441

365.2425 134.9859 93.0058 0.0003 -0.0003 -0.1000

365.2425 149.1825 89.4007 0.0003 -0.0001 -0.0395

365.2425 164.8721 83.3026 0.0003 -0.0002 -0.0706

365.2425 182.2119 76.7803 0.0003 -0.0002 -0.0815

365.2425 201.3753 72.1105 0.0003 -0.0002 -0.0627

365.2425 222.5541 69.9172 0.0003 -0.0001 -0.0309

365.2425 245.9603 68.4885 0.0003 -0.0001 -0.0206

price2ret assumes time units are days. Therefore, all durations are approximately 365 and the returns are normalized for that time unit.

Compute returns again, but specify that the observation times are years.

[Ryy,intervalsyy] = price2ret(S,Ticks=dates,Units="years");

[[NaN; intervalsyy] S [[NaN NaN]; Ryy] r2]ans = 10×6

NaN 100.0000 100.0000 NaN NaN 0

1.0000 110.5171 98.3541 0.1000 -0.0166 -0.0166

1.0000 122.1403 102.7850 0.1000 0.0441 0.0441

1.0000 134.9859 93.0058 0.1000 -0.1000 -0.1000

1.0000 149.1825 89.4007 0.1000 -0.0395 -0.0395

1.0000 164.8721 83.3026 0.1000 -0.0706 -0.0706

1.0000 182.2119 76.7803 0.1000 -0.0815 -0.0815

1.0000 201.3753 72.1105 0.1000 -0.0627 -0.0627

1.0000 222.5541 69.9172 0.1000 -0.0309 -0.0309

1.0000 245.9603 68.4885 0.1000 -0.0206 -0.0206

price2ret normalizes the returns relative to years, and now the returned rates match the simulated rates.

Complete the roundtrip by converting all returns series back to prices. Specify the returned observation intervals and the starting prices p1.

[P,ticks] = ret2price(R,Intervals=intervals,StartPrice=p1);

[Py,ticksy] = ret2price(Ry,Intervals=intervalsy,StartPrice=p1);

[Pyy,ticksyy] = ret2price(Ryy,Intervals=intervalsyy,StartPrice=p1,Units="years");

[ticks ticksy ticksyy]ans = 10×3

103 ×

0 0 0

0.0010 0.3652 0.0010

0.0020 0.7305 0.0020

0.0030 1.0957 0.0030

0.0040 1.4610 0.0040

0.0050 1.8262 0.0050

0.0060 2.1915 0.0060

0.0070 2.5567 0.0070

0.0080 2.9219 0.0080

0.0090 3.2872 0.0090

[S P Py Pyy]

ans = 10×8

100.0000 100.0000 100.0000 100.0000 100.0000 100.0000 100.0000 100.0000

110.5171 98.3541 110.5171 98.3541 110.5171 98.3541 110.5171 98.3541

122.1403 102.7850 122.1403 102.7850 122.1403 102.7850 122.1403 102.7850

134.9859 93.0058 134.9859 93.0058 134.9859 93.0058 134.9859 93.0058

149.1825 89.4007 149.1825 89.4007 149.1825 89.4007 149.1825 89.4007

164.8721 83.3026 164.8721 83.3026 164.8721 83.3026 164.8721 83.3026

182.2119 76.7803 182.2119 76.7803 182.2119 76.7803 182.2119 76.7803

201.3753 72.1105 201.3753 72.1105 201.3753 72.1105 201.3753 72.1105

222.5541 69.9172 222.5541 69.9172 222.5541 69.9172 222.5541 69.9172

245.9603 68.4885 245.9603 68.4885 245.9603 68.4885 245.9603 68.4885

Input Arguments

Name-Value Arguments

Output Arguments

Algorithms

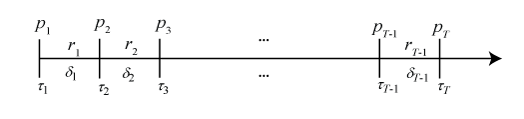

Consider the following variables:

The following figure shows how the inputs and outputs are associated.