Risk Model Validation

Validation metrics are fundamental tools for developing, validating, and monitoring risk models. Risk Management Toolbox™ provides a risk model validation namespace that includes a suite of data drift, discrimination, and calibration metrics. You can integrate these metrics into your credit and market risk workflows.

Functions

Featured Examples

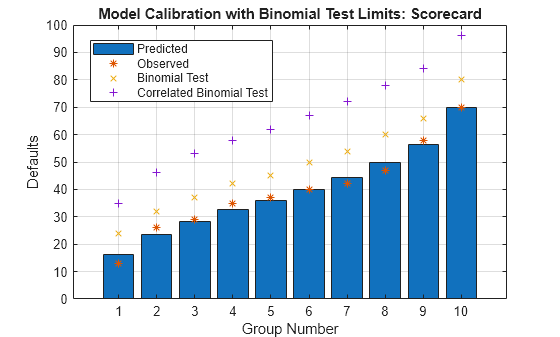

Credit Scoring Using Logistic Regression and Decision Trees

Create and compare two credit scoring models, which includes:

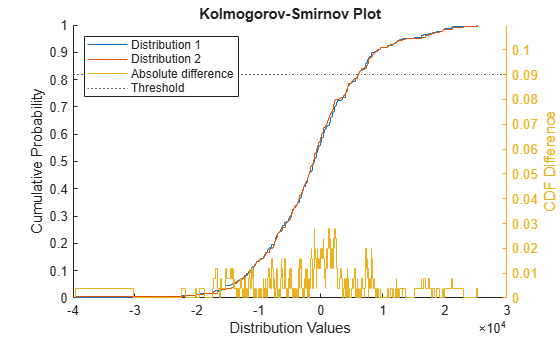

Perform Profit-and-Loss Attribution Test

Apply the Fundamental Review of the Trading Book (FRTB) profit-and-loss (P&L) attribution test to the recent trading history of a portfolio. The P&L attribution test determines whether two empirical distributions containing different P&L measures are similar enough for the measures to be considered equivalent for regulatory purposes. One distribution contains risk theoretical P&L (RTPL) values, which are the portfolio losses calculated by the trading desk's internal valuation model at the end of the trading period. The other distribution contains hypothetical P&L (HPL) values, which are the losses the portfolio would realize if the portfolio did not buy or sell any assets over the trading period. Profits are represented by negative P&L values.

Explore Fairness Metrics for Credit Scoring Model

Calculate and use data and model metrics to investigate the biases that exist in a model.

Interpretability and Explainability for Credit Scoring

Different techniques for interpreting and explaining the logic behind credit scoring predictions.