formatpoints

Format scorecard points and scaling

Description

sc = formatpoints(sc,Name,Value)

Examples

This example shows how to use formatpoints to scale by providing the points, odds levels, and PDO (points to double the odds). By using formatpoints to scale, you can put points and scores in a desired range that is more meaningful for practical purposes. Technically, this involves a linear transformation from the unscaled to the scaled points by the formatpoints function.

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011). Use the 'IDVar' argument in creditscorecard to indicate that 'CustID' contains ID information and should not be included as a predictor variable.

load CreditCardData sc = creditscorecard(data,'IDVar','CustID');

Perform automatic binning to bin for all predictors.

sc = autobinning(sc);

Fit a linear regression model using default parameters.

sc = fitmodel(sc);

1. Adding CustIncome, Deviance = 1490.8527, Chi2Stat = 32.588614, PValue = 1.1387992e-08

2. Adding TmWBank, Deviance = 1467.1415, Chi2Stat = 23.711203, PValue = 1.1192909e-06

3. Adding AMBalance, Deviance = 1455.5715, Chi2Stat = 11.569967, PValue = 0.00067025601

4. Adding EmpStatus, Deviance = 1447.3451, Chi2Stat = 8.2264038, PValue = 0.0041285257

5. Adding CustAge, Deviance = 1441.994, Chi2Stat = 5.3511754, PValue = 0.020708306

6. Adding ResStatus, Deviance = 1437.8756, Chi2Stat = 4.118404, PValue = 0.042419078

7. Adding OtherCC, Deviance = 1433.707, Chi2Stat = 4.1686018, PValue = 0.041179769

Generalized linear regression model:

logit(status) ~ 1 + CustAge + ResStatus + EmpStatus + CustIncome + TmWBank + OtherCC + AMBalance

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ ______ __________

(Intercept) 0.70239 0.064001 10.975 5.0538e-28

CustAge 0.60833 0.24932 2.44 0.014687

ResStatus 1.377 0.65272 2.1097 0.034888

EmpStatus 0.88565 0.293 3.0227 0.0025055

CustIncome 0.70164 0.21844 3.2121 0.0013179

TmWBank 1.1074 0.23271 4.7589 1.9464e-06

OtherCC 1.0883 0.52912 2.0569 0.039696

AMBalance 1.045 0.32214 3.2439 0.0011792

1200 observations, 1192 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 89.7, p-value = 1.4e-16

Display unscaled points for predictors retained in the fitting model and display the minimum and maximum possible unscaled scores.

[PointsInfo,MinScore,MaxScore] = displaypoints(sc)

PointsInfo=37×3 table

Predictors Bin Points

______________ ________________ _________

{'CustAge' } {'[-Inf,33)' } -0.15894

{'CustAge' } {'[33,37)' } -0.14036

{'CustAge' } {'[37,40)' } -0.060323

{'CustAge' } {'[40,46)' } 0.046408

{'CustAge' } {'[46,48)' } 0.21445

{'CustAge' } {'[48,58)' } 0.23039

{'CustAge' } {'[58,Inf]' } 0.479

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } -0.031252

{'ResStatus' } {'Home Owner' } 0.12696

{'ResStatus' } {'Other' } 0.37641

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } -0.076317

{'EmpStatus' } {'Employed' } 0.31449

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome'} {'[-Inf,29000)'} -0.45716

⋮

MinScore = -1.3100

MaxScore = 3.0726

Scale by providing the points, odds levels, and PDO (points to double the odds). Suppose that you want a score of 500 points to have odds of 2 (twice as likely to be good than to be bad) and that the odds double every 50 points (so that 550 points would have odds of 4).

sc = formatpoints(sc,'PointsOddsAndPDO',[500 2 50]);

[PointsInfo,MinScore,MaxScore] = displaypoints(sc)PointsInfo=37×3 table

Predictors Bin Points

______________ ________________ ______

{'CustAge' } {'[-Inf,33)' } 52.821

{'CustAge' } {'[33,37)' } 54.161

{'CustAge' } {'[37,40)' } 59.934

{'CustAge' } {'[40,46)' } 67.633

{'CustAge' } {'[46,48)' } 79.755

{'CustAge' } {'[48,58)' } 80.905

{'CustAge' } {'[58,Inf]' } 98.838

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } 62.031

{'ResStatus' } {'Home Owner' } 73.444

{'ResStatus' } {'Other' } 91.438

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } 58.781

{'EmpStatus' } {'Employed' } 86.971

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome'} {'[-Inf,29000)'} 31.309

⋮

MinScore = 355.5051

MaxScore = 671.6403

This example shows how to use formatpoints to scale by providing the Worst and Best score values. By using formatpoints to scale, you can put points and scores in a desired range that is more meaningful for practical purposes. Technically, this involves a linear transformation from the unscaled to the scaled points.

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011). Use the 'IDVar' argument in creditscorecard to indicate that 'CustID' contains ID information and should not be included as a predictor variable.

load CreditCardData sc = creditscorecard(data,'IDVar','CustID');

Perform automatic binning to bin for all predictors.

sc = autobinning(sc);

Fit a linear regression model using default parameters.

sc = fitmodel(sc);

1. Adding CustIncome, Deviance = 1490.8527, Chi2Stat = 32.588614, PValue = 1.1387992e-08

2. Adding TmWBank, Deviance = 1467.1415, Chi2Stat = 23.711203, PValue = 1.1192909e-06

3. Adding AMBalance, Deviance = 1455.5715, Chi2Stat = 11.569967, PValue = 0.00067025601

4. Adding EmpStatus, Deviance = 1447.3451, Chi2Stat = 8.2264038, PValue = 0.0041285257

5. Adding CustAge, Deviance = 1441.994, Chi2Stat = 5.3511754, PValue = 0.020708306

6. Adding ResStatus, Deviance = 1437.8756, Chi2Stat = 4.118404, PValue = 0.042419078

7. Adding OtherCC, Deviance = 1433.707, Chi2Stat = 4.1686018, PValue = 0.041179769

Generalized linear regression model:

logit(status) ~ 1 + CustAge + ResStatus + EmpStatus + CustIncome + TmWBank + OtherCC + AMBalance

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ ______ __________

(Intercept) 0.70239 0.064001 10.975 5.0538e-28

CustAge 0.60833 0.24932 2.44 0.014687

ResStatus 1.377 0.65272 2.1097 0.034888

EmpStatus 0.88565 0.293 3.0227 0.0025055

CustIncome 0.70164 0.21844 3.2121 0.0013179

TmWBank 1.1074 0.23271 4.7589 1.9464e-06

OtherCC 1.0883 0.52912 2.0569 0.039696

AMBalance 1.045 0.32214 3.2439 0.0011792

1200 observations, 1192 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 89.7, p-value = 1.4e-16

Display unscaled points for predictors retained in the fitting model and display the minimum and maximum possible unscaled scores.

[PointsInfo,MinScore,MaxScore] = displaypoints(sc)

PointsInfo=37×3 table

Predictors Bin Points

______________ ________________ _________

{'CustAge' } {'[-Inf,33)' } -0.15894

{'CustAge' } {'[33,37)' } -0.14036

{'CustAge' } {'[37,40)' } -0.060323

{'CustAge' } {'[40,46)' } 0.046408

{'CustAge' } {'[46,48)' } 0.21445

{'CustAge' } {'[48,58)' } 0.23039

{'CustAge' } {'[58,Inf]' } 0.479

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } -0.031252

{'ResStatus' } {'Home Owner' } 0.12696

{'ResStatus' } {'Other' } 0.37641

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } -0.076317

{'EmpStatus' } {'Employed' } 0.31449

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome'} {'[-Inf,29000)'} -0.45716

⋮

MinScore = -1.3100

MaxScore = 3.0726

Scale by providing the 'Worst' and 'Best' score values. The range provided below is a common score range. Display the points information again to verify that they are now scaled and also display the scaled minimum and maximum scores.

sc = formatpoints(sc,'WorstAndBestScores',[300 850]);

[PointsInfo,MinScore,MaxScore] = displaypoints(sc)PointsInfo=37×3 table

Predictors Bin Points

______________ ________________ ______

{'CustAge' } {'[-Inf,33)' } 46.396

{'CustAge' } {'[33,37)' } 48.727

{'CustAge' } {'[37,40)' } 58.772

{'CustAge' } {'[40,46)' } 72.167

{'CustAge' } {'[46,48)' } 93.256

{'CustAge' } {'[48,58)' } 95.256

{'CustAge' } {'[58,Inf]' } 126.46

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } 62.421

{'ResStatus' } {'Home Owner' } 82.276

{'ResStatus' } {'Other' } 113.58

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } 56.765

{'EmpStatus' } {'Employed' } 105.81

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome'} {'[-Inf,29000)'} 8.9706

⋮

MinScore = 300.0000

MaxScore = 850.0000

As expected, the values of MinScore and MaxScore correspond to the desired worst and best scores.

This example shows how to use formatpoints to scale by providing the Shift and Slope values. By using formatpoints to scale, you can put points and scores in a desired range that is more meaningful for practical purposes. Technically, this involves a linear transformation from the unscaled to the scaled points by the formatpoints function.

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011). Use the 'IDVar' argument in creditscorecard to indicate that 'CustID' contains ID information and should not be included as a predictor variable.

load CreditCardData sc = creditscorecard(data,'IDVar','CustID');

Perform automatic binning to bin for all predictors.

sc = autobinning(sc);

Fit a linear regression model using default parameters.

sc = fitmodel(sc);

1. Adding CustIncome, Deviance = 1490.8527, Chi2Stat = 32.588614, PValue = 1.1387992e-08

2. Adding TmWBank, Deviance = 1467.1415, Chi2Stat = 23.711203, PValue = 1.1192909e-06

3. Adding AMBalance, Deviance = 1455.5715, Chi2Stat = 11.569967, PValue = 0.00067025601

4. Adding EmpStatus, Deviance = 1447.3451, Chi2Stat = 8.2264038, PValue = 0.0041285257

5. Adding CustAge, Deviance = 1441.994, Chi2Stat = 5.3511754, PValue = 0.020708306

6. Adding ResStatus, Deviance = 1437.8756, Chi2Stat = 4.118404, PValue = 0.042419078

7. Adding OtherCC, Deviance = 1433.707, Chi2Stat = 4.1686018, PValue = 0.041179769

Generalized linear regression model:

logit(status) ~ 1 + CustAge + ResStatus + EmpStatus + CustIncome + TmWBank + OtherCC + AMBalance

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ ______ __________

(Intercept) 0.70239 0.064001 10.975 5.0538e-28

CustAge 0.60833 0.24932 2.44 0.014687

ResStatus 1.377 0.65272 2.1097 0.034888

EmpStatus 0.88565 0.293 3.0227 0.0025055

CustIncome 0.70164 0.21844 3.2121 0.0013179

TmWBank 1.1074 0.23271 4.7589 1.9464e-06

OtherCC 1.0883 0.52912 2.0569 0.039696

AMBalance 1.045 0.32214 3.2439 0.0011792

1200 observations, 1192 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 89.7, p-value = 1.4e-16

Display unscaled points for predictors retained in the fitting model and display the minimum and maximum possible unscaled scores.

[PointsInfo,MinScore,MaxScore] = displaypoints(sc)

PointsInfo=37×3 table

Predictors Bin Points

______________ ________________ _________

{'CustAge' } {'[-Inf,33)' } -0.15894

{'CustAge' } {'[33,37)' } -0.14036

{'CustAge' } {'[37,40)' } -0.060323

{'CustAge' } {'[40,46)' } 0.046408

{'CustAge' } {'[46,48)' } 0.21445

{'CustAge' } {'[48,58)' } 0.23039

{'CustAge' } {'[58,Inf]' } 0.479

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } -0.031252

{'ResStatus' } {'Home Owner' } 0.12696

{'ResStatus' } {'Other' } 0.37641

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } -0.076317

{'EmpStatus' } {'Employed' } 0.31449

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome'} {'[-Inf,29000)'} -0.45716

⋮

MinScore = -1.3100

MaxScore = 3.0726

Scale by providing the 'Shift' and 'Slope' values. In this example, there is an arbitrary choice of shift and slope. Display the points information again to verify that they are now scaled and also display the scaled minimum and maximum scores.

sc = formatpoints(sc,'ShiftAndSlope',[300 6]);

[PointsInfo,MinScore,MaxScore] = displaypoints(sc)PointsInfo=37×3 table

Predictors Bin Points

______________ ________________ ______

{'CustAge' } {'[-Inf,33)' } 41.904

{'CustAge' } {'[33,37)' } 42.015

{'CustAge' } {'[37,40)' } 42.495

{'CustAge' } {'[40,46)' } 43.136

{'CustAge' } {'[46,48)' } 44.144

{'CustAge' } {'[48,58)' } 44.239

{'CustAge' } {'[58,Inf]' } 45.731

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } 42.67

{'ResStatus' } {'Home Owner' } 43.619

{'ResStatus' } {'Other' } 45.116

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } 42.399

{'EmpStatus' } {'Employed' } 44.744

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome'} {'[-Inf,29000)'} 40.114

⋮

MinScore = 292.1401

MaxScore = 318.4355

This example shows how to use formatpoints to separate the base points from the rest of the points assigned to each predictor variable. The formatpoints name-value pair argument 'BasePoints' serves this purpose.

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011). Use the 'IDVar' argument in creditscorecard to indicate that 'CustID' contains ID information and should not be included as a predictor variable.

load CreditCardData sc = creditscorecard(data,'IDVar','CustID');

Perform automatic binning to bin for all predictors.

sc = autobinning(sc);

Fit a linear regression model using default parameters.

sc = fitmodel(sc);

1. Adding CustIncome, Deviance = 1490.8527, Chi2Stat = 32.588614, PValue = 1.1387992e-08

2. Adding TmWBank, Deviance = 1467.1415, Chi2Stat = 23.711203, PValue = 1.1192909e-06

3. Adding AMBalance, Deviance = 1455.5715, Chi2Stat = 11.569967, PValue = 0.00067025601

4. Adding EmpStatus, Deviance = 1447.3451, Chi2Stat = 8.2264038, PValue = 0.0041285257

5. Adding CustAge, Deviance = 1441.994, Chi2Stat = 5.3511754, PValue = 0.020708306

6. Adding ResStatus, Deviance = 1437.8756, Chi2Stat = 4.118404, PValue = 0.042419078

7. Adding OtherCC, Deviance = 1433.707, Chi2Stat = 4.1686018, PValue = 0.041179769

Generalized linear regression model:

logit(status) ~ 1 + CustAge + ResStatus + EmpStatus + CustIncome + TmWBank + OtherCC + AMBalance

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ ______ __________

(Intercept) 0.70239 0.064001 10.975 5.0538e-28

CustAge 0.60833 0.24932 2.44 0.014687

ResStatus 1.377 0.65272 2.1097 0.034888

EmpStatus 0.88565 0.293 3.0227 0.0025055

CustIncome 0.70164 0.21844 3.2121 0.0013179

TmWBank 1.1074 0.23271 4.7589 1.9464e-06

OtherCC 1.0883 0.52912 2.0569 0.039696

AMBalance 1.045 0.32214 3.2439 0.0011792

1200 observations, 1192 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 89.7, p-value = 1.4e-16

Display unscaled points for predictors retained in the fitting model and display the minimum and maximum possible unscaled scores.

[PointsInfo,MinScore,MaxScore] = displaypoints(sc)

PointsInfo=37×3 table

Predictors Bin Points

______________ ________________ _________

{'CustAge' } {'[-Inf,33)' } -0.15894

{'CustAge' } {'[33,37)' } -0.14036

{'CustAge' } {'[37,40)' } -0.060323

{'CustAge' } {'[40,46)' } 0.046408

{'CustAge' } {'[46,48)' } 0.21445

{'CustAge' } {'[48,58)' } 0.23039

{'CustAge' } {'[58,Inf]' } 0.479

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } -0.031252

{'ResStatus' } {'Home Owner' } 0.12696

{'ResStatus' } {'Other' } 0.37641

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } -0.076317

{'EmpStatus' } {'Employed' } 0.31449

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome'} {'[-Inf,29000)'} -0.45716

⋮

MinScore = -1.3100

MaxScore = 3.0726

By setting the name-value pair argument BasePoints to true, the points information table reports the base points separately in the first row. The minimum and maximum possible scores are not affected by this option.

sc = formatpoints(sc,'BasePoints',true);

[PointsInfo,MinScore,MaxScore] = displaypoints(sc)PointsInfo=38×3 table

Predictors Bin Points

______________ ______________ _________

{'BasePoints'} {'BasePoints'} 0.70239

{'CustAge' } {'[-Inf,33)' } -0.25928

{'CustAge' } {'[33,37)' } -0.24071

{'CustAge' } {'[37,40)' } -0.16066

{'CustAge' } {'[40,46)' } -0.053933

{'CustAge' } {'[46,48)' } 0.11411

{'CustAge' } {'[48,58)' } 0.13005

{'CustAge' } {'[58,Inf]' } 0.37866

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } -0.13159

{'ResStatus' } {'Home Owner'} 0.026616

{'ResStatus' } {'Other' } 0.27607

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } -0.17666

{'EmpStatus' } {'Employed' } 0.21415

{'EmpStatus' } {'<missing>' } NaN

⋮

MinScore = -1.3100

MaxScore = 3.0726

This example shows how to use formatpoints to round points. Rounding is usually applied after scaling, otherwise, if the points for a particular predictor are all in a small range, rounding could cause the rounded points for different bins to be the same. Also, rounding all the points may slightly change the minimum and maximum total points.

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011). Use the 'IDVar' argument in creditscorecard to indicate that 'CustID' contains ID information and should not be included as a predictor variable.

load CreditCardData sc = creditscorecard(data,'IDVar','CustID');

Perform automatic binning to bin for all predictors.

sc = autobinning(sc);

Fit a linear regression model using default parameters.

sc = fitmodel(sc);

1. Adding CustIncome, Deviance = 1490.8527, Chi2Stat = 32.588614, PValue = 1.1387992e-08

2. Adding TmWBank, Deviance = 1467.1415, Chi2Stat = 23.711203, PValue = 1.1192909e-06

3. Adding AMBalance, Deviance = 1455.5715, Chi2Stat = 11.569967, PValue = 0.00067025601

4. Adding EmpStatus, Deviance = 1447.3451, Chi2Stat = 8.2264038, PValue = 0.0041285257

5. Adding CustAge, Deviance = 1441.994, Chi2Stat = 5.3511754, PValue = 0.020708306

6. Adding ResStatus, Deviance = 1437.8756, Chi2Stat = 4.118404, PValue = 0.042419078

7. Adding OtherCC, Deviance = 1433.707, Chi2Stat = 4.1686018, PValue = 0.041179769

Generalized linear regression model:

logit(status) ~ 1 + CustAge + ResStatus + EmpStatus + CustIncome + TmWBank + OtherCC + AMBalance

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ ______ __________

(Intercept) 0.70239 0.064001 10.975 5.0538e-28

CustAge 0.60833 0.24932 2.44 0.014687

ResStatus 1.377 0.65272 2.1097 0.034888

EmpStatus 0.88565 0.293 3.0227 0.0025055

CustIncome 0.70164 0.21844 3.2121 0.0013179

TmWBank 1.1074 0.23271 4.7589 1.9464e-06

OtherCC 1.0883 0.52912 2.0569 0.039696

AMBalance 1.045 0.32214 3.2439 0.0011792

1200 observations, 1192 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 89.7, p-value = 1.4e-16

Display unscaled points for predictors retained in the fitting model and display the minimum and maximum possible unscaled scores.

[PointsInfo,MinScore,MaxScore] = displaypoints(sc)

PointsInfo=37×3 table

Predictors Bin Points

______________ ________________ _________

{'CustAge' } {'[-Inf,33)' } -0.15894

{'CustAge' } {'[33,37)' } -0.14036

{'CustAge' } {'[37,40)' } -0.060323

{'CustAge' } {'[40,46)' } 0.046408

{'CustAge' } {'[46,48)' } 0.21445

{'CustAge' } {'[48,58)' } 0.23039

{'CustAge' } {'[58,Inf]' } 0.479

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } -0.031252

{'ResStatus' } {'Home Owner' } 0.12696

{'ResStatus' } {'Other' } 0.37641

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } -0.076317

{'EmpStatus' } {'Employed' } 0.31449

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome'} {'[-Inf,29000)'} -0.45716

⋮

MinScore = -1.3100

MaxScore = 3.0726

Scale points, and display the points information. By default, no rounding is applied.

sc = formatpoints(sc,'WorstAndBestScores',[300 850]);

PointsInfo = displaypoints(sc)PointsInfo=37×3 table

Predictors Bin Points

______________ ________________ ______

{'CustAge' } {'[-Inf,33)' } 46.396

{'CustAge' } {'[33,37)' } 48.727

{'CustAge' } {'[37,40)' } 58.772

{'CustAge' } {'[40,46)' } 72.167

{'CustAge' } {'[46,48)' } 93.256

{'CustAge' } {'[48,58)' } 95.256

{'CustAge' } {'[58,Inf]' } 126.46

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } 62.421

{'ResStatus' } {'Home Owner' } 82.276

{'ResStatus' } {'Other' } 113.58

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } 56.765

{'EmpStatus' } {'Employed' } 105.81

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome'} {'[-Inf,29000)'} 8.9706

⋮

Use the name-value pair argument Round to apply rounding for all points and then display the points information again.

sc = formatpoints(sc,'Round','AllPoints'); PointsInfo = displaypoints(sc)

PointsInfo=37×3 table

Predictors Bin Points

______________ ________________ ______

{'CustAge' } {'[-Inf,33)' } 46

{'CustAge' } {'[33,37)' } 49

{'CustAge' } {'[37,40)' } 59

{'CustAge' } {'[40,46)' } 72

{'CustAge' } {'[46,48)' } 93

{'CustAge' } {'[48,58)' } 95

{'CustAge' } {'[58,Inf]' } 126

{'CustAge' } {'<missing>' } NaN

{'ResStatus' } {'Tenant' } 62

{'ResStatus' } {'Home Owner' } 82

{'ResStatus' } {'Other' } 114

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } 57

{'EmpStatus' } {'Employed' } 106

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome'} {'[-Inf,29000)'} 9

⋮

This example shows that rounding scorecard points can modify the original risk ranking of a credit scorecard. You can control rounding by using formatpoints with the optional name-value pair argument for 'Rounding'.

Credit scores rank customers by risk. If higher scores are given to better, less risky customers, then higher scores must correspond to lower default probabilities. When you use the name-value pair argument for 'Rounding', depending on the value for 'Rounding', the rounding behavior is:

When

'Rounding'is set to'None'(default option), no rounding is applied to points or scores, and the risk ranking is completely consistent with the calibrated model.When

'Rounding'is set to'FinalScore', rounding is only applied to the final scores. In this case: a) Customers with different scores (different risk) may have the same rounded score. b) Customers with the same rounded score may have different default probabilities. c) Customer with higher rounded scores will always have lower default probability than customers with lower scores.When

'Rounding'is set to'AllPoints', rounding is applied to all points in the scorecard (all bins, all predictors). In this case: a) Customers with different scores (different risk) may have the same rounded score, or their ranking may even be reversed (the customer with the lower original score may have a higher rounded score). b) Customers with the same rounded score may have different default probabilities. c) Customer with higher rounded scores may in some cases have higher default probabilities than customers with lower scores.

Create a creditscorecard

To demonstrate the rounding behavior, first create a creditscorecard object.

load CreditCardData sc = creditscorecard(data,'IDVar','CustID','ResponseVar','status'); sc = autobinning(sc); sc = modifybins(sc,'CustIncome','CutPoints',20000:5000:60000); sc = fitmodel(sc);

1. Adding CustIncome, Deviance = 1487.9719, Chi2Stat = 35.469392, PValue = 2.5909009e-09

2. Adding TmWBank, Deviance = 1465.7998, Chi2Stat = 22.172089, PValue = 2.4927133e-06

3. Adding AMBalance, Deviance = 1455.206, Chi2Stat = 10.593833, PValue = 0.0011346548

4. Adding EmpStatus, Deviance = 1446.3918, Chi2Stat = 8.8142314, PValue = 0.0029889009

5. Adding CustAge, Deviance = 1440.6825, Chi2Stat = 5.709236, PValue = 0.016875883

6. Adding ResStatus, Deviance = 1436.1363, Chi2Stat = 4.5462043, PValue = 0.032991806

7. Adding OtherCC, Deviance = 1431.9546, Chi2Stat = 4.1817827, PValue = 0.040860699

Generalized linear regression model:

logit(status) ~ 1 + CustAge + ResStatus + EmpStatus + CustIncome + TmWBank + OtherCC + AMBalance

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ ______ __________

(Intercept) 0.70247 0.064046 10.968 5.4345e-28

CustAge 0.60579 0.24405 2.4822 0.013058

ResStatus 1.4463 0.65427 2.2105 0.02707

EmpStatus 0.90501 0.29262 3.0928 0.0019828

CustIncome 0.70869 0.20535 3.4512 0.00055815

TmWBank 1.0839 0.23244 4.6631 3.1145e-06

OtherCC 1.0906 0.52936 2.0602 0.039377

AMBalance 1.0148 0.32273 3.1445 0.0016636

1200 observations, 1192 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 91.5, p-value = 6.12e-17

Apply the 'Rounding' Options

Apply each of the three 'Rounding' options to the creditscorecard object.

sc = formatpoints(sc,'PointsOddsAndPDO',[500 2 50]); % No Rounding points1 = displaypoints(sc); [S1,P1] = score(sc); defProb1 = probdefault(sc); sc = formatpoints(sc,'Round','AllPoints'); % 'AllPoints' Rounding points2 = displaypoints(sc); [S2,P2] = score(sc); defProb2 = probdefault(sc); sc = formatpoints(sc,'Round','FinalScore'); % 'FinalScore' Rounding points3 = displaypoints(sc); [S3,P3] = score(sc); defProb3 = probdefault(sc);

Compare the 'Rounding' Options

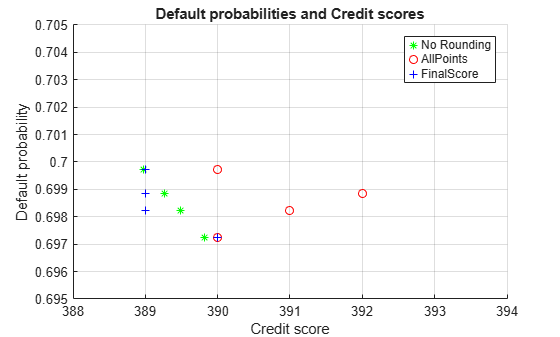

Visualize the default probabilities versus the scores.

figure hold on scatter(S1, defProb1, 'g*') scatter(S2, defProb2, 'ro') scatter(S3, defProb3, 'b+') legend('No Rounding','AllPoints','FinalScore') axis([388 394 0.695 0.705]) xlabel('Credit score') ylabel('Default probability') title('Default probabilities and Credit scores') grid

Inspect the points and total scores for each 'Rounding' option, in table format.

ind = [208 363 694 886]; ProbDefault = defProb1(ind)

ProbDefault = 4×1

0.6997

0.6989

0.6982

0.6972

% ScoreNoRounding = S1(ind)

PointsNoRounding = P1(ind,:);

PointsNoRounding.Total = S1(ind)PointsNoRounding=4×8 table

CustAge ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance Total

_______ _________ _________ __________ _______ _______ _________ ______

52.9 61.555 58.503 24.647 51.551 50.416 89.4 388.97

67.65 61.555 58.503 24.647 51.551 75.723 49.64 389.27

54.234 61.555 58.503 24.647 51.551 75.723 63.271 389.48

52.9 92.441 58.503 24.647 61.277 50.416 49.64 389.82

% ScoreAllPoints = S2(ind)

PointsAllPoints = P2(ind,:);

PointsAllPoints.Total = S2(ind)PointsAllPoints=4×8 table

CustAge ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance Total

_______ _________ _________ __________ _______ _______ _________ _____

53 62 59 25 52 50 89 390

68 62 59 25 52 76 50 392

54 62 59 25 52 76 63 391

53 92 59 25 61 50 50 390

% ScoreFinalScore = S3(ind)

PointsFinalScore = P3(ind,:);

PointsFinalScore.Total = S3(ind)PointsFinalScore=4×8 table

CustAge ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance Total

_______ _________ _________ __________ _______ _______ _________ _____

52.9 61.555 58.503 24.647 51.551 50.416 89.4 389

67.65 61.555 58.503 24.647 51.551 75.723 49.64 389

54.234 61.555 58.503 24.647 51.551 75.723 63.271 389

52.9 92.441 58.503 24.647 61.277 50.416 49.64 390

The original creditscorecard model, without rounding, was calibrated to the data with a logistic regression. The ranking and probabilities have a statistical foundation.

Rounding, however, effectively modifies the creditscorecard model. When only the final score is rounded, this leads to some "ties" in rounded scores, but at least the risk ranking across scores is preserved (because if s1 <= s2, then round(s1) <= round(s2)).

However, when you round all points, a score may gain extra points by chance. For example, in the second row in the table (row 363 of original data), the points for all predictors are rounded up by almost 0.5. The original score is 389.27. Rounding the final score makes it 389. However, rounding all points makes it 392, that is three points higher than rounding the final score.

This example shows how to use formatpoints to score missing or out-of-range data. When data is scored, some observations can be either missing (NaN, or undefined) or out of range. You will need to decide whether or not points are assigned to these cases. Use the name-value pair argument Missing to do so.

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011). Use the 'IDVar' argument in creditscorecard to indicate that 'CustID' contains ID information and should not be included as a predictor variable.

load CreditCardData sc = creditscorecard(data,'IDVar','CustID');

Perform automatic binning to bin for all predictors.

sc = autobinning(sc);

Indicate that the minimum allowed value for 'CustAge' is zero. This makes any negative values for age invalid or out-of-range.

sc = modifybins(sc,'CustAge','MinValue',0);

Fit a linear regression model using default parameters.

sc = fitmodel(sc);

1. Adding CustIncome, Deviance = 1490.8527, Chi2Stat = 32.588614, PValue = 1.1387992e-08

2. Adding TmWBank, Deviance = 1467.1415, Chi2Stat = 23.711203, PValue = 1.1192909e-06

3. Adding AMBalance, Deviance = 1455.5715, Chi2Stat = 11.569967, PValue = 0.00067025601

4. Adding EmpStatus, Deviance = 1447.3451, Chi2Stat = 8.2264038, PValue = 0.0041285257

5. Adding CustAge, Deviance = 1441.994, Chi2Stat = 5.3511754, PValue = 0.020708306

6. Adding ResStatus, Deviance = 1437.8756, Chi2Stat = 4.118404, PValue = 0.042419078

7. Adding OtherCC, Deviance = 1433.707, Chi2Stat = 4.1686018, PValue = 0.041179769

Generalized linear regression model:

logit(status) ~ 1 + CustAge + ResStatus + EmpStatus + CustIncome + TmWBank + OtherCC + AMBalance

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ ______ __________

(Intercept) 0.70239 0.064001 10.975 5.0538e-28

CustAge 0.60833 0.24932 2.44 0.014687

ResStatus 1.377 0.65272 2.1097 0.034888

EmpStatus 0.88565 0.293 3.0227 0.0025055

CustIncome 0.70164 0.21844 3.2121 0.0013179

TmWBank 1.1074 0.23271 4.7589 1.9464e-06

OtherCC 1.0883 0.52912 2.0569 0.039696

AMBalance 1.045 0.32214 3.2439 0.0011792

1200 observations, 1192 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 89.7, p-value = 1.4e-16

Suppose there are missing or out of range observations in the data that you want to score. Notice that by default, the points and score assigned to the missing value is NaN.

% Set up a data set with missing and out of range data for illustration purposes newdata = data(1:5,:); newdata.CustAge(1) = NaN; % missing newdata.CustAge(2) = -100; % invalid newdata.ResStatus(3) = missing; % missing newdata.ResStatus(4) = 'House'; % invalid disp(newdata)

CustID CustAge TmAtAddress ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance UtilRate status

______ _______ ___________ ___________ _________ __________ _______ _______ _________ ________ ______

1 NaN 62 Tenant Unknown 50000 55 Yes 1055.9 0.22 0

2 -100 22 Home Owner Employed 52000 25 Yes 1161.6 0.24 0

3 47 30 <undefined> Employed 37000 61 No 877.23 0.29 0

4 50 75 House Employed 53000 20 Yes 157.37 0.08 0

5 68 56 Home Owner Employed 53000 14 Yes 561.84 0.11 0

[Scores,Points] = score(sc,newdata); disp(Scores)

NaN

NaN

NaN

NaN

1.4535

disp(Points)

CustAge ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance

_______ _________ _________ __________ _________ ________ _________

NaN -0.031252 -0.076317 0.43693 0.39607 0.15842 -0.017472

NaN 0.12696 0.31449 0.43693 -0.033752 0.15842 -0.017472

0.21445 NaN 0.31449 0.081611 0.39607 -0.19168 -0.017472

0.23039 NaN 0.31449 0.43693 -0.044811 0.15842 0.35551

0.479 0.12696 0.31449 0.43693 -0.044811 0.15842 -0.017472

Use the name-value pair argument Missing to replace NaN with points corresponding to a zero Weight-of-Evidence (WOE).

sc = formatpoints(sc,'Missing','ZeroWOE'); [Scores,Points] = score(sc,newdata); disp(Scores)

0.9667

1.0859

0.8978

1.5513

1.4535

disp(Points)

CustAge ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance

_______ _________ _________ __________ _________ ________ _________

0.10034 -0.031252 -0.076317 0.43693 0.39607 0.15842 -0.017472

0.10034 0.12696 0.31449 0.43693 -0.033752 0.15842 -0.017472

0.21445 0.10034 0.31449 0.081611 0.39607 -0.19168 -0.017472

0.23039 0.10034 0.31449 0.43693 -0.044811 0.15842 0.35551

0.479 0.12696 0.31449 0.43693 -0.044811 0.15842 -0.017472

Alternatively, use the name-value pair argument Missing to replace the missing value with the minimum points for the predictors that have the missing values.

sc = formatpoints(sc,'Missing','MinPoints'); [Scores,Points] = score(sc,newdata); disp(Scores)

0.7074

0.8266

0.7662

1.4197

1.4535

disp(Points)

CustAge ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance

________ _________ _________ __________ _________ ________ _________

-0.15894 -0.031252 -0.076317 0.43693 0.39607 0.15842 -0.017472

-0.15894 0.12696 0.31449 0.43693 -0.033752 0.15842 -0.017472

0.21445 -0.031252 0.31449 0.081611 0.39607 -0.19168 -0.017472

0.23039 -0.031252 0.31449 0.43693 -0.044811 0.15842 0.35551

0.479 0.12696 0.31449 0.43693 -0.044811 0.15842 -0.017472

As a third alternative, use the name-value pair argument Missing to replace the missing value with the maximum points for the predictors that have the missing values.

sc = formatpoints(sc,'Missing','MaxPoints'); [Scores,Points] = score(sc,newdata); disp(Scores)

1.3454

1.4646

1.1739

1.8273

1.4535

disp(Points)

CustAge ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance

_______ _________ _________ __________ _________ ________ _________

0.479 -0.031252 -0.076317 0.43693 0.39607 0.15842 -0.017472

0.479 0.12696 0.31449 0.43693 -0.033752 0.15842 -0.017472

0.21445 0.37641 0.31449 0.081611 0.39607 -0.19168 -0.017472

0.23039 0.37641 0.31449 0.43693 -0.044811 0.15842 0.35551

0.479 0.12696 0.31449 0.43693 -0.044811 0.15842 -0.017472

Verify that the minimum and maximum points assigned to the missing data correspond to the minimum and maximum points for the corresponding predictors. The points for 'CustAge' are reported in the first seven rows of the points information table. For 'ResStatus' the points are in rows 8 through 10.

PointsInfo = displaypoints(sc); PointsInfo(1:7,:)

ans=7×3 table

Predictors Bin Points

___________ ____________ _________

{'CustAge'} {'[0,33)' } -0.15894

{'CustAge'} {'[33,37)' } -0.14036

{'CustAge'} {'[37,40)' } -0.060323

{'CustAge'} {'[40,46)' } 0.046408

{'CustAge'} {'[46,48)' } 0.21445

{'CustAge'} {'[48,58)' } 0.23039

{'CustAge'} {'[58,Inf]'} 0.479

min(PointsInfo.Points(1:7))

ans = -0.1589

max(PointsInfo.Points(1:7))

ans = 0.4790

PointsInfo(8:10,:)

ans=3×3 table

Predictors Bin Points

_____________ ______________ _________

{'CustAge' } {'<missing>' } 0.479

{'ResStatus'} {'Tenant' } -0.031252

{'ResStatus'} {'Home Owner'} 0.12696

min(PointsInfo.Points(8:10))

ans = -0.0313

max(PointsInfo.Points(8:10))

ans = 0.4790

This example describes the assignment of points for missing data when the 'BinMissingData' option is set to true.

Predictors that have missing data in the training set have an explicit bin for

<missing>with corresponding points in the final scorecard. These points are computed from the Weight-of-Evidence (WOE) value for the<missing>bin and the logistic model coefficients. For scoring purposes, these points are assigned to missing values and to out-of-range values.Predictors with no missing data in the training set have no

<missing>bin, therefore no WOE can be estimated from the training data. By default, the points for missing and out-of-range values are set toNaN, and this leads to a score ofNaNwhen runningscore. For predictors that have no explicit<missing>bin, use the name-value argument'Missing'informatpointsto indicate how missing data should be treated for scoring purposes.

Create a creditscorecard object using the CreditCardData.mat file to load the dataMissing with missing values.

load CreditCardData.mat

head(dataMissing,5) CustID CustAge TmAtAddress ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance UtilRate status

______ _______ ___________ ___________ _________ __________ _______ _______ _________ ________ ______

1 53 62 <undefined> Unknown 50000 55 Yes 1055.9 0.22 0

2 61 22 Home Owner Employed 52000 25 Yes 1161.6 0.24 0

3 47 30 Tenant Employed 37000 61 No 877.23 0.29 0

4 NaN 75 Home Owner Employed 53000 20 Yes 157.37 0.08 0

5 68 56 Home Owner Employed 53000 14 Yes 561.84 0.11 0

fprintf('Number of rows: %d\n',height(dataMissing))Number of rows: 1200

fprintf('Number of missing values CustAge: %d\n',sum(ismissing(dataMissing.CustAge)))Number of missing values CustAge: 30

fprintf('Number of missing values ResStatus: %d\n',sum(ismissing(dataMissing.ResStatus)))Number of missing values ResStatus: 40

Use creditscorecard with the name-value argument 'BinMissingData' set to true to bin the missing numeric or categorical data in a separate bin. Apply automatic binning.

sc = creditscorecard(dataMissing,'IDVar','CustID','BinMissingData',true); sc = autobinning(sc); disp(sc)

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustAge' 'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

CategoricalPredictors: {'ResStatus' 'EmpStatus' 'OtherCC'}

BinMissingData: 1

IDVar: 'CustID'

PredictorVars: {'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate'}

Data: [1200×11 table]

Set a minimum value of zero for CustAge and CustIncome. With this, any negative age or income information becomes invalid or "out-of-range". For scoring purposes, out-of-range values are given the same points as missing values.

sc = modifybins(sc,'CustAge','MinValue',0); sc = modifybins(sc,'CustIncome','MinValue',0);

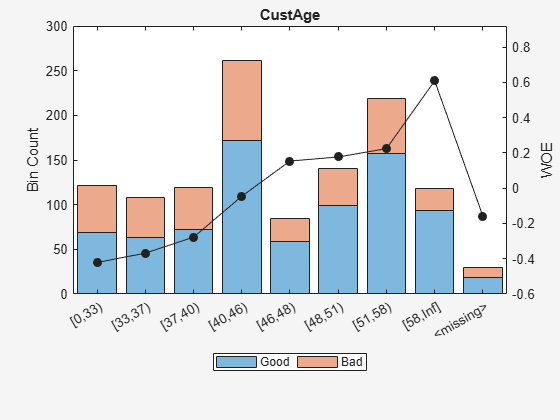

Display and plot bin information for numeric data for 'CustAge' that includes missing data in a separate bin labelled <missing>.

[bi,cp] = bininfo(sc,'CustAge');

disp(bi) Bin Good Bad Odds WOE InfoValue

_____________ ____ ___ ______ ________ __________

{'[0,33)' } 69 52 1.3269 -0.42156 0.018993

{'[33,37)' } 63 45 1.4 -0.36795 0.012839

{'[37,40)' } 72 47 1.5319 -0.2779 0.0079824

{'[40,46)' } 172 89 1.9326 -0.04556 0.0004549

{'[46,48)' } 59 25 2.36 0.15424 0.0016199

{'[48,51)' } 99 41 2.4146 0.17713 0.0035449

{'[51,58)' } 157 62 2.5323 0.22469 0.0088407

{'[58,Inf]' } 93 25 3.72 0.60931 0.032198

{'<missing>'} 19 11 1.7273 -0.15787 0.00063885

{'Totals' } 803 397 2.0227 NaN 0.087112

plotbins(sc,'CustAge')

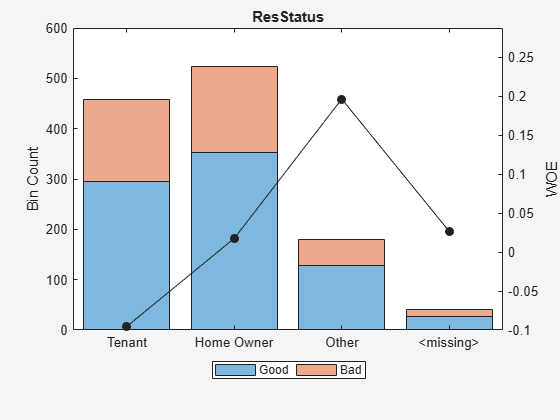

Display and plot bin information for categorical data for 'ResStatus' that includes missing data in a separate bin labelled <missing>.

[bi,cg] = bininfo(sc,'ResStatus');

disp(bi) Bin Good Bad Odds WOE InfoValue

______________ ____ ___ ______ _________ __________

{'Tenant' } 296 161 1.8385 -0.095463 0.0035249

{'Home Owner'} 352 171 2.0585 0.017549 0.00013382

{'Other' } 128 52 2.4615 0.19637 0.0055808

{'<missing>' } 27 13 2.0769 0.026469 2.3248e-05

{'Totals' } 803 397 2.0227 NaN 0.0092627

plotbins(sc,'ResStatus')

For the 'CustAge' and 'ResStatus' predictors, there is missing data (NaNs and <undefined>) in the training data, and the binning process estimates a WOE value of -0.15787 and 0.026469 respectively for missing data in these predictors, as shown above.

For EmpStatus and CustIncome there is no explicit bin for missing values because the training data has no missing values for these predictors.

bi = bininfo(sc,'EmpStatus');

disp(bi) Bin Good Bad Odds WOE InfoValue

____________ ____ ___ ______ ________ _________

{'Unknown' } 396 239 1.6569 -0.19947 0.021715

{'Employed'} 407 158 2.5759 0.2418 0.026323

{'Totals' } 803 397 2.0227 NaN 0.048038

bi = bininfo(sc,'CustIncome');

disp(bi) Bin Good Bad Odds WOE InfoValue

_________________ ____ ___ _______ _________ __________

{'[0,29000)' } 53 58 0.91379 -0.79457 0.06364

{'[29000,33000)'} 74 49 1.5102 -0.29217 0.0091366

{'[33000,35000)'} 68 36 1.8889 -0.06843 0.00041042

{'[35000,40000)'} 193 98 1.9694 -0.026696 0.00017359

{'[40000,42000)'} 68 34 2 -0.011271 1.0819e-05

{'[42000,47000)'} 164 66 2.4848 0.20579 0.0078175

{'[47000,Inf]' } 183 56 3.2679 0.47972 0.041657

{'Totals' } 803 397 2.0227 NaN 0.12285

Use fitmodel to fit a logistic regression model using Weight of Evidence (WOE) data. fitmodel internally transforms all the predictor variables into WOE values, using the bins found with the automatic binning process. fitmodel then fits a logistic regression model using a stepwise method (by default). For predictors that have missing data, there is an explicit <missing> bin, with a corresponding WOE value computed from the data. When using fitmodel, the corresponding WOE value for the <missing> bin is applied when performing the WOE transformation.

[sc,mdl] = fitmodel(sc);

1. Adding CustIncome, Deviance = 1490.8527, Chi2Stat = 32.588614, PValue = 1.1387992e-08

2. Adding TmWBank, Deviance = 1467.1415, Chi2Stat = 23.711203, PValue = 1.1192909e-06

3. Adding AMBalance, Deviance = 1455.5715, Chi2Stat = 11.569967, PValue = 0.00067025601

4. Adding EmpStatus, Deviance = 1447.3451, Chi2Stat = 8.2264038, PValue = 0.0041285257

5. Adding CustAge, Deviance = 1442.8477, Chi2Stat = 4.4974731, PValue = 0.033944979

6. Adding ResStatus, Deviance = 1438.9783, Chi2Stat = 3.86941, PValue = 0.049173805

7. Adding OtherCC, Deviance = 1434.9751, Chi2Stat = 4.0031966, PValue = 0.045414057

Generalized linear regression model:

logit(status) ~ 1 + CustAge + ResStatus + EmpStatus + CustIncome + TmWBank + OtherCC + AMBalance

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ ______ __________

(Intercept) 0.70229 0.063959 10.98 4.7498e-28

CustAge 0.57421 0.25708 2.2335 0.025513

ResStatus 1.3629 0.66952 2.0356 0.04179

EmpStatus 0.88373 0.2929 3.0172 0.002551

CustIncome 0.73535 0.2159 3.406 0.00065929

TmWBank 1.1065 0.23267 4.7556 1.9783e-06

OtherCC 1.0648 0.52826 2.0156 0.043841

AMBalance 1.0446 0.32197 3.2443 0.0011775

1200 observations, 1192 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 88.5, p-value = 2.55e-16

Scale the scorecard points by the "points, odds, and points to double the odds (PDO)" method using the 'PointsOddsAndPDO' argument of formatpoints. Suppose that you want a score of 500 points to have odds of 2 (twice as likely to be good than to be bad) and that the odds double every 50 points (so that 550 points would have odds of 4).

Display the scorecard showing the scaled points for predictors retained in the fitting model.

sc = formatpoints(sc,'PointsOddsAndPDO',[500 2 50]);

PointsInfo = displaypoints(sc)PointsInfo=38×3 table

Predictors Bin Points

_____________ ______________ ______

{'CustAge' } {'[0,33)' } 54.062

{'CustAge' } {'[33,37)' } 56.282

{'CustAge' } {'[37,40)' } 60.012

{'CustAge' } {'[40,46)' } 69.636

{'CustAge' } {'[46,48)' } 77.912

{'CustAge' } {'[48,51)' } 78.86

{'CustAge' } {'[51,58)' } 80.83

{'CustAge' } {'[58,Inf]' } 96.76

{'CustAge' } {'<missing>' } 64.984

{'ResStatus'} {'Tenant' } 62.138

{'ResStatus'} {'Home Owner'} 73.248

{'ResStatus'} {'Other' } 90.828

{'ResStatus'} {'<missing>' } 74.125

{'EmpStatus'} {'Unknown' } 58.807

{'EmpStatus'} {'Employed' } 86.937

{'EmpStatus'} {'<missing>' } NaN

⋮

Notice that points for the <missing> bin for CustAge and ResStatus are explicitly shown (as 64.9836 and 74.1250, respectively). These points are computed from the WOE value for the <missing> bin, and the logistic model coefficients.

For predictors that have no missing data in the training set, there is no explicit <missing> bin. By default the points are set to NaN for missing data and they lead to a score of NaN when running score. For predictors that have no explicit <missing> bin, use the name-value argument 'Missing' in formatpoints to indicate how missing data should be treated for scoring purposes.

For the purpose of illustration, take a few rows from the original data as test data and introduce some missing data. Also introduce some invalid, or out-of-range values. For numeric data, values below the minimum (or above the maximum) allowed are considered invalid, such as a negative value for age (recall 'MinValue' was earlier set to 0 for CustAge and CustIncome). For categorical data, invalid values are categories not explicitly included in the scorecard, for example, a residential status not previously mapped to scorecard categories, such as "House", or a meaningless string such as "abc123".

tdata = dataMissing(11:18,mdl.PredictorNames); % Keep only the predictors retained in the model % Set some missing values tdata.CustAge(1) = NaN; tdata.ResStatus(2) = missing; tdata.EmpStatus(3) = missing; tdata.CustIncome(4) = NaN; % Set some invalid values tdata.CustAge(5) = -100; tdata.ResStatus(6) = 'House'; tdata.EmpStatus(7) = 'Freelancer'; tdata.CustIncome(8) = -1; disp(tdata)

CustAge ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance

_______ ___________ ___________ __________ _______ _______ _________

NaN Tenant Unknown 34000 44 Yes 119.8

48 <undefined> Unknown 44000 14 Yes 403.62

65 Home Owner <undefined> 48000 6 No 111.88

44 Other Unknown NaN 35 No 436.41

-100 Other Employed 46000 16 Yes 162.21

33 House Employed 36000 36 Yes 845.02

39 Tenant Freelancer 34000 40 Yes 756.26

24 Home Owner Employed -1 19 Yes 449.61

Score the new data and see how points are assigned for missing CustAge and ResStatus, because we have an explicit bin with points for <missing>. However, for EmpStatus and CustIncome the score function sets the points to NaN.

[Scores,Points] = score(sc,tdata); disp(Scores)

481.2231

520.8353

NaN

NaN

551.7922

487.9588

NaN

NaN

disp(Points)

CustAge ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance

_______ _________ _________ __________ _______ _______ _________

64.984 62.138 58.807 67.893 61.858 75.622 89.922

78.86 74.125 58.807 82.439 61.061 75.622 89.922

96.76 73.248 NaN 96.969 51.132 50.914 89.922

69.636 90.828 58.807 NaN 61.858 50.914 89.922

64.984 90.828 86.937 82.439 61.061 75.622 89.922

56.282 74.125 86.937 70.107 61.858 75.622 63.028

60.012 62.138 NaN 67.893 61.858 75.622 63.028

54.062 73.248 86.937 NaN 61.061 75.622 89.922

Use the name-value argument 'Missing' in formatpoints to choose how to assign points to missing values for predictors that do not have an explicit <missing> bin. In this example, use the 'MinPoints' option for the 'Missing' argument. The minimum points for EmpStatus in the scorecard displayed above are 58.8072, and for CustIncome the minimum points are 29.3753.

sc = formatpoints(sc,'Missing','MinPoints'); [Scores,Points] = score(sc,tdata); disp(Scores)

481.2231 520.8353 517.7532 451.3405 551.7922 487.9588 449.3577 470.2267

disp(Points)

CustAge ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance

_______ _________ _________ __________ _______ _______ _________

64.984 62.138 58.807 67.893 61.858 75.622 89.922

78.86 74.125 58.807 82.439 61.061 75.622 89.922

96.76 73.248 58.807 96.969 51.132 50.914 89.922

69.636 90.828 58.807 29.375 61.858 50.914 89.922

64.984 90.828 86.937 82.439 61.061 75.622 89.922

56.282 74.125 86.937 70.107 61.858 75.622 63.028

60.012 62.138 58.807 67.893 61.858 75.622 63.028

54.062 73.248 86.937 29.375 61.061 75.622 89.922

Input Arguments

Name-Value Arguments

Output Arguments

Algorithms

The score of an individual i is given by the formula

Score(i) = Shift + Slope*(b0 + b1*WOE1(i) + b2*WOE2(i)+ ... +bp*WOEp(i))

where bj is the coefficient of the jth

variable in the model, and WOEj(i) is the Weight

of Evidence (WOE) value for the ith individual corresponding to the

jth model variable. Shift and

Slope are scaling constants further discussed below. The scaling

constant can be controlled with formatpoints.

If the data for individual i is in the i-th

row of a given dataset, to compute a score, the

data(i,j) is binned using existing binning

maps, and converted into a corresponding Weight of Evidence value

WOEj(i). Using the

model coefficients, the unscaled score is computed

as

s = b0 + b1*WOE1(i) + ... +bp*WOEp(i).

For simplicity, assume in the description above that the j-th variable in the model is the j-th column in the data input, although, in general, the order of variables in a given dataset does not have to match the order of variables in the model, and the dataset could have additional variables that are not used in the model.

The formatting options can be controlled using formatpoints.

When the base points are reported separately (see the formatpoints

parameter BasePoints), the base points are given

by

Base Points = Shift + Slope*b0,

Points_ji = Slope*(bj*WOEj(i))).

By default, the base points are not reported separately, in which case

Points_ji = (Shift + Slope*b0)/p + Slope*(bj*WOEj(i)),

By default, no rounding is applied to the points by the score

function (Round is None). If

Round is set to AllPoints using

formatpoints, then the points for individual i

for variable j are given

by

points if rounding is 'AllPoints': round( Points_ji )

Round is

set to FinalScore using formatpoints, then the

points per predictor are not rounded, and only the final score is

roundedscore if rounding is 'FinalScore': round(Score(i)).

Regarding the scaling parameters, the Shift parameter, and the

Slope parameter can be set directly with the

ShiftAndSlope parameter of formatpoints.

Alternatively, you can use the formatpoints parameter for

WorstAndBestScores. In this case, the parameters

Shift and Slope are found internally by

solving the

system

Shift + Slope*smin = WorstScore, Shift + Slope*smax = BestScore,

WorstScore and BestScore are the first and

second elements in the formatpoints parameter for

WorstAndBestScores and smin and

smax are the minimum and maximum possible unscaled

scores:smin = b0 + min(b1*WOE1) + ... +min(bp*WOEp), smax = b0 + max(b1*WOE1) + ... +max(bp*WOEp).

A third alternative to scale scores is the PointsOddsAndPDO

parameter in formatpoints. In this case, assume that the unscaled

score s gives the log-odds for a row, and the

Shift and Slope parameters are found by

solving the following

system

Points = Shift + Slope*log(Odds) Points + PDO = Shift + Slope*log(2*Odds)

Points, Odds, and PDO

("points to double the odds") are the first, second, and third elements in the

PointsOddsAndPDO parameter.Whenever a given dataset has a missing or out-of-range value data

(i,j), the points for predictor

j, for individual i, are set to

NaN by default, which results in a missing score for that row (a

NaN score). Using the Missing parameter for

formatpoints, you can modify this behavior and set the

corresponding Weight-of-Evidence (WOE) value to zero, or set the points to the minimum

points, or the maximum points for that predictor.

References

[1] Anderson, R. The Credit Scoring Toolkit. Oxford University Press, 2007.

[2] Refaat, M. Credit Risk Scorecards: Development and Implementation Using SAS. lulu.com, 2011.

Version History

Introduced in R2014b

See Also

creditscorecard | autobinning | bininfo | predictorinfo | modifypredictor | plotbins | modifybins | bindata | fitmodel | displaypoints | score | setmodel | probdefault | validatemodel