What Is Current Expected Credit Loss (CECL)?

The current expected credit loss model is a standard that governs how financial institutions recognize credit losses on financial instruments. Introduced by the Financial Accounting Standards Board (FASB) through ASU 2016-13, CECL aims to address the limitations of the previous incurred loss model under US GAAP.

Key Objectives of the CECL Model

The CECL model is intended to:

- Enable timely recognition of credit losses: It requires entities to recognize an allowance for lifetime expected credit losses, rather than waiting for a loss event to occur. This proactive approach aims to eliminate delays in loss recognition.

- Reduce complexity: By decreasing the number of credit impairment models, CECL simplifies the accounting for credit losses across different types of financial instruments.

- Provide flexibility in estimation methods: The standard does not mandate a specific method for estimating expected credit losses, allowing entities to choose an approach that best fits their circumstances.

Applicability of CECL Beyond Banks

While the CECL standard—a mandatory accounting requirement for all entities that follow US GAAP—primarily affects banks, it also applies to nonbank entities that hold financial instruments such as trade receivables, lease receivables, and held-to-maturity debt securities. Nonbanks need to assess which of their assets fall under the CECL model and adjust their credit impairment models accordingly.

Expected Losses vs. Incurred Losses

Unlike previous models, CECL does not set a threshold for impairment recognition, the process of identifying and accounting for a reduction in the value of an asset. Instead, entities must estimate expected credit losses over the life of the financial asset, considering all relevant information, including historical data, current conditions, and reasonable forecasts.

Lifetime Loss Estimates

CECL requires entities to estimate losses over the contractual life of a financial asset, factoring in expected prepayments and considering all available relevant information. However, entities are not required to forecast beyond the period for which they can make reasonable and supportable predictions.

MATLAB for CECL

MATLAB® offers a comprehensive suite of tools to implement CECL standards efficiently. With MATLAB, financial institutions can perform:

- Credit risk modeling: Develop probability of default (PD), loss given default (LGD), and exposure at default (EAD) models to accurately estimate ECL.

- Macroeconomic forecasting: Predict economic conditions affecting credit risk.

- Scenario generation: Develop various financial scenarios to assess risk.

- Instrument pricing: Evaluate the risk sensitivity of financial instruments.

- Automated reporting: Streamline reporting with integrated point-in-time (PIT) model and data selection.

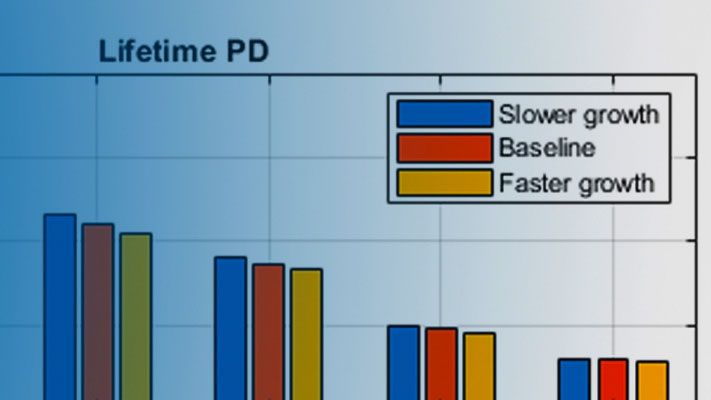

Visualizing loan-level results for PD, LGD, and EAD using Risk Management Toolbox. (See MATLAB code.)

For more detail on implementing current expected credit loss with MATLAB, see Risk Management Toolbox™, Statistics and Machine Learning Toolbox™, Econometrics Toolbox™, and MATLAB Report Generator™.

Examples and How To

Software Reference

See also: Monte Carlo simulation, credit scoring model, risk management solutions, IFRS 9, expected credit loss, Basel IV, fraud analytics