creditDefaultCopula

Create creditDefaultCopula object to simulate and analyze

multifactor credit default model

Description

The creditDefaultCopula class simulates portfolio

losses due to counterparty defaults using a multifactor model.

creditDefaultCopula associates each counterparty with a

random variable, called a latent variable, which is mapped to default/non-default

outcomes for each scenario such that defaults occur with probability

PD. In the event of default, a loss for that scenario is

recorded equal to EAD * LGD for the

counterparty. These latent variables are simulated using a multi-factor model, where

systemic credit fluctuations are modeled with a series of risk factors. These

factors can be based on industry sectors (such as financial, aerospace),

geographical regions (such as USA, Eurozone), or any other underlying driver of

credit risk. Each counterparty is assigned a series of weights which determine their

sensitivity to each underlying credit factors.

The inputs to the model describe the credit-sensitive portfolio of exposures:

EAD— Exposure at defaultPD— Probability of defaultLGD— Loss given default (1 - Recovery)Weights— Factor and idiosyncratic model weights

After the creditDefaultCopula object is created (see Create creditDefaultCopula and Properties), use the simulate function to simulate credit defaults using the multifactor

model. The results are stored in the form of a distribution of losses at the

portfolio and counterparty level. Several risk measures at the portfolio level are

calculated, and the risk contributions from individual obligors. The model calculates:

Full simulated distribution of portfolio losses across scenarios

Losses on each counterparty across scenarios

Several risk measures (

VaR,CVaR,EL,Std) with confidence intervalsRisk contributions per counterparty (for

ELandCVaR)

Creation

Description

cdc = creditDefaultCopula(EAD,PD,LGD,Weights)creditDefaultCopula object. The

creditDefaultCopula object has the following properties:

A table with the following variables (each row of the table represents one counterparty):

ID— ID to identify each counterpartyEAD— Exposure at defaultPD— Probability of defaultLGD— Loss given defaultWeights— Factor and idiosyncratic weights for counterparties

Factor correlation matrix, a

NumFactors-by-NumFactorsmatrix that defines the correlation between the risk factors.The value-at-risk level, used when reporting VaR and CVaR.

Portfolio losses, a

NumScenarios-by-1vector of portfolio losses. This property is empty until thesimulatefunction is used.

cdc = creditDefaultCopula(___,Name,Value)cdc =

creditDefaultCopula(EAD,PD,LGD,Weights,'VaRLevel',0.99). You

can specify multiple name-value pairs as optional name-value pair arguments.

Input Arguments

Name-Value Arguments

Properties

Object Functions

simulate | Simulate credit defaults using a creditDefaultCopula

object |

portfolioRisk | Generate portfolio-level risk measurements |

riskContribution | Generate risk contributions for each counterparty in portfolio |

confidenceBands | Confidence interval bands |

getScenarios | Counterparty scenarios |

Examples

Load saved portfolio data.

load CreditPortfolioData.mat;Create a creditDefaultCopula object with a two-factor model.

cdc = creditDefaultCopula(EAD,PD,LGD,Weights2F,'FactorCorrelation',FactorCorr2F)cdc =

creditDefaultCopula with properties:

Portfolio: [100×5 table]

FactorCorrelation: [2×2 double]

VaRLevel: 0.9500

UseParallel: "off"

PortfolioLosses: []

Set the VaRLevel to 99%.

cdc.VaRLevel = 0.99;

Simulate 100,000 scenarios, and view the portfolio risk measures.

cdc = simulate(cdc,1e5)

cdc =

creditDefaultCopula with properties:

Portfolio: [100×5 table]

FactorCorrelation: [2×2 double]

VaRLevel: 0.9900

UseParallel: "off"

PortfolioLosses: [30.1008 3.6910 3.2895 19.2151 7.5761 44.5088 19.5419 1.7909 72.1443 12.6933 36.0228 1.7909 4.8512 23.0230 54.0877 35.9298 35.3757 26.1678 36.8868 24.6242 2.9770 15.3030 0 0 10.5546 61.2268 32.5802 42.5504 … ] (1×100000 double)

portRisk = portfolioRisk(cdc)

portRisk=1×4 table

EL Std VaR CVaR

______ ______ _____ ______

24.876 23.778 102.4 121.28

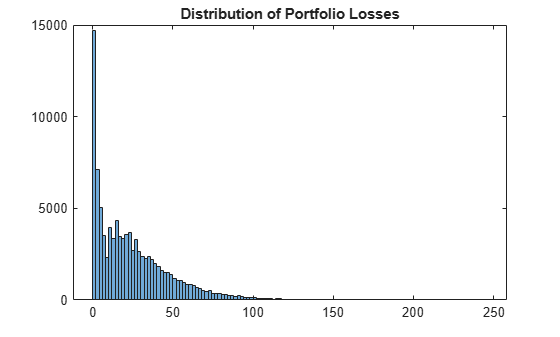

View a histogram of the portfolio losses.

histogram(cdc.PortfolioLosses);

title('Distribution of Portfolio Losses');

For further analysis, use the simulate, portfolioRisk, riskContribution, and getScenarios functions with the creditDefaultCopula object.

References

[1] Crouhy, M., Galai, D., and Mark, R. “A Comparative Analysis of Current Credit Risk Models.” Journal of Banking and Finance. Vol. 24, 2000, pp. 59 – 117.

[2] Gordy, M. “A Comparative Anatomy of Credit Risk Models.” Journal of Banking and Finance. Vol. 24, 2000, pp. 119 – 149.

[3] Gupton, G., Finger, C., and Bhatia, M. “CreditMetrics – Technical Document.” J. P. Morgan, New York, 1997.

[4] Jorion, P. Financial Risk Manager Handbook. 6th Edition. Wiley Finance, 2011.

[5] Löffler, G., and Posch, P. Credit Risk Modeling Using Excel and VBA. Wiley Finance, 2007.

[6] McNeil, A., Frey, R., and Embrechts, P. Quantitative Risk Management: Concepts, Techniques, and Tools. Princeton University Press, 2005.

Extended Capabilities

Version History

Introduced in R2017aSee Also

table | simulate | portfolioRisk | riskContribution | confidenceBands | getScenarios | creditMigrationCopula | nearcorr