fitNelsonSiegel

Fit Nelson-Siegel function to bond market data

fitNelsonSiegel for an IRFunctionCurve is not

recommended. Use fitNelsonSiegel with a

parametercurve object instead.

For more information, see fitNelsonSiegel.

Syntax

Description

CurveObj = IRFunctionCurve.fitNelsonSiegel(Type,Settle,Instruments)

CurveObj = IRFunctionCurve.fitNelsonSiegel(___,Name,Value)

Examples

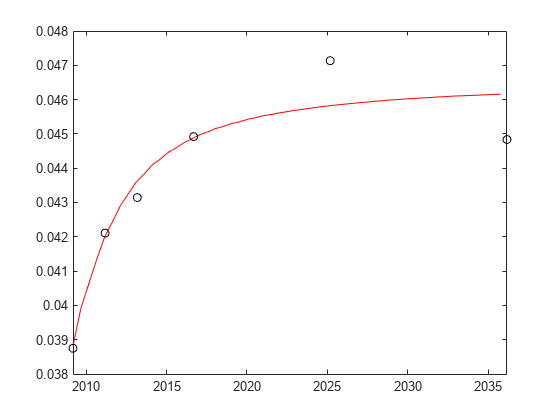

This example shows how to use the Nelson-Siegel function to fit bond market data.

Settle = repmat(datenum('30-Apr-2008'),[6 1]); Maturity = [datenum('07-Mar-2009');datenum('07-Mar-2011');... datenum('07-Mar-2013');datenum('07-Sep-2016');... datenum('07-Mar-2025');datenum('07-Mar-2036')]; CleanPrice = [100.1;100.1;100.8;96.6;103.3;96.3]; CouponRate = [0.0400;0.0425;0.0450;0.0400;0.0500;0.0425]; Instruments = [Settle Maturity CleanPrice CouponRate]; PlottingPoints = datenum('07-Mar-2009'):180:datenum('07-Mar-2036'); Yield = bndyield(CleanPrice,CouponRate,Settle,Maturity); NSModel = IRFunctionCurve.fitNelsonSiegel('Zero',datenum('30-Apr-2008'),Instruments); NSModel.Parameters

ans = 1×4

4.6617 -1.0227 -0.3482 1.2387

% Create the plot plot(datetime(PlottingPoints,"ConvertFrom","datenum"), getParYields(NSModel, PlottingPoints),'r') hold on scatter(datetime(Maturity,"ConvertFrom","datenum"),Yield,'black')

Input Arguments

Name-Value Arguments

Output Arguments

Algorithms

The Nelson-Siegel model proposes that the instantaneous forward curve can be modeled with the following:

This can be integrated to derive an equation for the zero curve (see [6] for more information on the equations and the derivation):

See [1] for more information.

References

[1] Nelson, C.R., Siegel, A.F. “Parsimonious modelling of yield curves.” Journal of Business. Vol. 60, 1987, pp 473–89.

[2] Svensson, L.E.O. “Estimating and interpreting forward interest rates: Sweden 1992-4.” International Monetary Fund, IMF Working Paper, 1994/114.

[3] Fisher, M., Nychka, D., Zervos, D. “Fitting the term structure of interest rates with smoothing splines.” Board of Governors of the Federal Reserve System, Federal Reserve Board Working Paper 1995-1.

[4] Anderson, N., Sleath, J. “New estimates of the UK real and nominal yield curves.” Bank of England Quarterly Bulletin, November, 1999, pp 384–92.

[5] Waggoner, D. “Spline Methods for Extracting Interest Rate Curves from Coupon Bond Prices.” Federal Reserve Board Working Paper 1997–10.

[6] “Zero-coupon yield curves: technical documentation.” BIS Papers No. 25, October 2005.

[7] Bolder, D.J., Gusba, S. “Exponentials, Polynomials, and Fourier Series: More Yield Curve Modelling at the Bank of Canada.” Working Papers 2002–29, Bank of Canada.

[8] Bolder, D.J., Streliski, D. “Yield Curve Modelling at the Bank of Canada.” Technical Reports 84, 1999, Bank of Canada.

Version History

Introduced in R2008b

See Also

IRFitOptions | IRFunctionCurve | fitSvensson | fitSmoothingSpline | fitFunction

Topics

- Fitting IRFunctionCurve Object Using Nelson-Siegel Method

- Fitting Interest-Rate Curve Functions

- Using fitFunction to Create Custom Fitting Function

- Interest-Rate Curve Objects and Workflow

- Creating Interest-Rate Curve Objects

- Mapping Financial Instruments Toolbox Curve Functions to Object-Based Framework