transprob

Estimate transition probabilities from credit ratings data

Syntax

Description

[

constructs a transition matrix from historical data of credit ratings.transMat,sampleTotals,idTotals] = transprob(data)

[

adds optional name-value pair arguments. transMat,sampleTotals,idTotals] = transprob(___,Name,Value)

Examples

Using the historical credit rating table as input data from Data_TransProb.mat display the first ten rows and compute the transition matrix:

load Data_TransProb

data(1:10,:)ans=10×3 table

ID Date Rating

____________ _______________ _______

{'00010283'} {'10-Nov-1984'} {'CCC'}

{'00010283'} {'12-May-1986'} {'B' }

{'00010283'} {'29-Jun-1988'} {'CCC'}

{'00010283'} {'12-Dec-1991'} {'D' }

{'00013326'} {'09-Feb-1985'} {'A' }

{'00013326'} {'24-Feb-1994'} {'AA' }

{'00013326'} {'10-Nov-2000'} {'BBB'}

{'00014413'} {'23-Dec-1982'} {'B' }

{'00014413'} {'20-Apr-1988'} {'BB' }

{'00014413'} {'16-Jan-1998'} {'B' }

% Estimate transition probabilities with default settings

transMat = transprob(data)transMat = 8×8

93.1170 5.8428 0.8232 0.1763 0.0376 0.0012 0.0001 0.0017

1.6166 93.1518 4.3632 0.6602 0.1626 0.0055 0.0004 0.0396

0.1237 2.9003 92.2197 4.0756 0.5365 0.0661 0.0028 0.0753

0.0236 0.2312 5.0059 90.1846 3.7979 0.4733 0.0642 0.2193

0.0216 0.1134 0.6357 5.7960 88.9866 3.4497 0.2919 0.7050

0.0010 0.0062 0.1081 0.8697 7.3366 86.7215 2.5169 2.4399

0.0002 0.0011 0.0120 0.2582 1.4294 4.2898 81.2927 12.7167

0 0 0 0 0 0 0 100.0000

Using the historical credit rating table input data from Data_TransProb.mat, compute the transition matrix using the cohort algorithm:

%Estimate transition probabilities with 'cohort' algorithm transMatCoh = transprob(data,'algorithm','cohort')

transMatCoh = 8×8

93.1345 5.9335 0.7456 0.1553 0.0311 0 0 0

1.7359 92.9198 4.5446 0.6046 0.1560 0 0 0.0390

0.1268 2.9716 91.9913 4.3124 0.4711 0.0544 0 0.0725

0.0210 0.3785 5.0683 89.7792 4.0379 0.4627 0.0421 0.2103

0.0221 0.1105 0.6851 6.2320 88.3757 3.6464 0.2873 0.6409

0 0 0.0761 0.7230 7.9909 86.1872 2.7397 2.2831

0 0 0 0.3094 1.8561 4.5630 80.8971 12.3743

0 0 0 0 0 0 0 100.0000

Using the historical credit rating data with ratings investment grade ('IG'), speculative grade ('SG'), and default ('D'), from Data_TransProb.mat display the first ten rows and compute the transition matrix:

dataIGSG(1:10,:)

ans=10×3 table

ID Date Rating

____________ _______________ ______

{'00011253'} {'04-Apr-1983'} {'IG'}

{'00012751'} {'17-Feb-1985'} {'SG'}

{'00012751'} {'19-May-1986'} {'D' }

{'00014690'} {'17-Jan-1983'} {'IG'}

{'00012144'} {'21-Nov-1984'} {'IG'}

{'00012144'} {'25-Mar-1992'} {'SG'}

{'00012144'} {'07-May-1994'} {'IG'}

{'00012144'} {'23-Jan-2000'} {'SG'}

{'00012144'} {'20-Aug-2001'} {'IG'}

{'00012937'} {'07-Feb-1984'} {'IG'}

transMatIGSG = transprob(dataIGSG,'labels',{'IG','SG','D'})

transMatIGSG = 3×3

98.6719 1.2020 0.1261

3.5781 93.3318 3.0901

0 0 100.0000

Using the historical credit rating data with numeric ratings for investment grade (1), speculative grade (2), and default (3), from Data_TransProb.mat display the first ten rows and compute the transition matrix:

dataIGSGnum(1:10,:)

ans=10×3 table

ID Date Rating

____________ _______________ ______

{'00011253'} {'04-Apr-1983'} 1

{'00012751'} {'17-Feb-1985'} 2

{'00012751'} {'19-May-1986'} 3

{'00014690'} {'17-Jan-1983'} 1

{'00012144'} {'21-Nov-1984'} 1

{'00012144'} {'25-Mar-1992'} 2

{'00012144'} {'07-May-1994'} 1

{'00012144'} {'23-Jan-2000'} 2

{'00012144'} {'20-Aug-2001'} 1

{'00012937'} {'07-Feb-1984'} 1

transMatIGSGnum = transprob(dataIGSGnum,'labels',{1,2,3})transMatIGSGnum = 3×3

98.6719 1.2020 0.1261

3.5781 93.3318 3.0901

0 0 100.0000

Using a MATLAB® table containing the historical credit rating cell array input data (dataCellFormat) from Data_TransProb.mat, estimate the transition probabilities with default settings.

load Data_TransProb

transMat = transprob(dataCellFormat)transMat = 8×8

93.1170 5.8428 0.8232 0.1763 0.0376 0.0012 0.0001 0.0017

1.6166 93.1518 4.3632 0.6602 0.1626 0.0055 0.0004 0.0396

0.1237 2.9003 92.2197 4.0756 0.5365 0.0661 0.0028 0.0753

0.0236 0.2312 5.0059 90.1846 3.7979 0.4733 0.0642 0.2193

0.0216 0.1134 0.6357 5.7960 88.9866 3.4497 0.2919 0.7050

0.0010 0.0062 0.1081 0.8697 7.3366 86.7215 2.5169 2.4399

0.0002 0.0011 0.0120 0.2582 1.4294 4.2898 81.2927 12.7167

0 0 0 0 0 0 0 100.0000

Using the historical credit rating cell array input data (dataCellFormat), compute the transition matrix using the cohort algorithm:

%Estimate transition probabilities with 'cohort' algorithm transMatCoh = transprob(dataCellFormat,'algorithm','cohort')

transMatCoh = 8×8

93.1345 5.9335 0.7456 0.1553 0.0311 0 0 0

1.7359 92.9198 4.5446 0.6046 0.1560 0 0 0.0390

0.1268 2.9716 91.9913 4.3124 0.4711 0.0544 0 0.0725

0.0210 0.3785 5.0683 89.7792 4.0379 0.4627 0.0421 0.2103

0.0221 0.1105 0.6851 6.2320 88.3757 3.6464 0.2873 0.6409

0 0 0.0761 0.7230 7.9909 86.1872 2.7397 2.2831

0 0 0 0.3094 1.8561 4.5630 80.8971 12.3743

0 0 0 0 0 0 0 100.0000

This example shows how to visualize credit rating transitions that are used as an input to the transprob function. The example also describes how the transprob function treats rating transitions when the company data starts after the start date of the analysis, or when the end date of the analysis is after the last transition observed.

Sample Data

Set up fictitious sample data for illustration purposes.

data = {'ABC','17-Feb-2015','AA';

'ABC','6-Jul-2017','A';

'LMN','12-Aug-2014','B';

'LMN','9-Nov-2015','CCC';

'LMN','7-Sep-2016','D';

'XYZ','14-May-2013','BB';

'XYZ','21-Jun-2016','BBB'};

data = cell2table(data,'VariableNames',{'ID','Date','Rating'});

disp(data) ID Date Rating

_______ _______________ _______

{'ABC'} {'17-Feb-2015'} {'AA' }

{'ABC'} {'6-Jul-2017' } {'A' }

{'LMN'} {'12-Aug-2014'} {'B' }

{'LMN'} {'9-Nov-2015' } {'CCC'}

{'LMN'} {'7-Sep-2016' } {'D' }

{'XYZ'} {'14-May-2013'} {'BB' }

{'XYZ'} {'21-Jun-2016'} {'BBB'}

The transprob function understands that this panel-data format indicates the dates when a new rating is assigned to a given company. transprob assumes that such ratings remain unchanged, unless a subsequent row explicitly indicates a rating change. For example, for company 'ABC', transprob understands that the 'A' rating is unchanged for any date after '6-Jul-2017' (indefinitely).

Compute Transition Matrix and Transition Counts

The transprob function returns a transition probability matrix as the primary output. There are also optional outputs that contain additional information for how many transitions occurred. For more information, see transprob for information on the optional outputs for both the 'cohort' and the 'duration' methods.

For illustration purposes, this example allows you to pick the StartYear (limited to 2014 or 2015 for this example) and the EndYear (2016 or 2017). This example also uses the hDisplayTransitions helper function (see the Local Functions section) to format the transitions information for ease of reading.

StartYear =2014; EndYear =

2017; startDate = datetime(StartYear,12,31,'Locale','en_US'); endDate = datetime(EndYear,12,31,'Locale','en_US'); RatingLabels = ["AAA","AA","A","BBB","BB","B","CCC","D"]; [tm,st,it] = transprob(data,'startDate',startDate,'endDate',endDate,'algorithm','cohort','labels',RatingLabels);

The transition probabilities of the TransMat output indicate the probability of migrating between ratings. The probabilities are expressed in %, that is, they are multiplied by 100.

hDisplayTransitions(tm,RatingLabels,"Transition Matrix")Transition Matrix

AAA AA A BBB BB B CCC D

___ __ ___ ___ __ _ ___ ___

AAA 100 0 0 0 0 0 0 0

AA 0 50 50 0 0 0 0 0

A 0 0 100 0 0 0 0 0

BBB 0 0 0 100 0 0 0 0

BB 0 0 0 50 50 0 0 0

B 0 0 0 0 0 0 100 0

CCC 0 0 0 0 0 0 0 100

D 0 0 0 0 0 0 0 100

The transition counts are stored in the sampleTotals optional output and indicate how many transitions occurred between ratings for the entire sample (that is, all companies).

hDisplayTransitions(st.totalsMat,RatingLabels,"Transition counts, all companies")Transition counts, all companies

AAA AA A BBB BB B CCC D

___ __ _ ___ __ _ ___ _

AAA 0 0 0 0 0 0 0 0

AA 0 1 1 0 0 0 0 0

A 0 0 0 0 0 0 0 0

BBB 0 0 0 1 0 0 0 0

BB 0 0 0 1 1 0 0 0

B 0 0 0 0 0 0 1 0

CCC 0 0 0 0 0 0 0 1

D 0 0 0 0 0 0 0 1

The third output of transprob is idTotals that contains information about transitions at an ID level, company by company (in the same order that the companies appear in the input data).

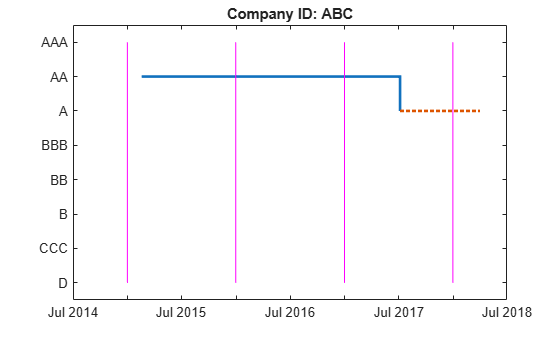

Select a company to display the transition counts and a corresponding visualization of the transitions. The hPlotTransitions helper function (see the Local Functions section) shows the transitions history for a company.

CompanyID ="ABC"; UniqueIDs = unique(data.ID,'stable'); [~,CompanyIndex] = ismember(CompanyID,UniqueIDs); hDisplayTransitions(it(CompanyIndex).totalsMat,RatingLabels,strcat("Transition counts, company ID: ",CompanyID))

Transition counts, company ID: ABC

AAA AA A BBB BB B CCC D

___ __ _ ___ __ _ ___ _

AAA 0 0 0 0 0 0 0 0

AA 0 1 1 0 0 0 0 0

A 0 0 0 0 0 0 0 0

BBB 0 0 0 0 0 0 0 0

BB 0 0 0 0 0 0 0 0

B 0 0 0 0 0 0 0 0

CCC 0 0 0 0 0 0 0 0

D 0 0 0 0 0 0 0 0

hPlotTransitions(CompanyID,startDate,endDate,data,RatingLabels)

To understand how transprob handles data when the first observed date is after the start date of the analysis, or whose last observed date occurs before the end date of the analysis, consider the following example. For company 'ABC' suppose that the analysis has a start date of 31-Dec-2014 and end date of 31-Dec-2017. There are only two transitions reported for this company for that analysis time window. The first observation for 'ABC' happened on 17-Feb-2015. So the 31-Dec-2015 snapshot is the first time the company is observed. By 31-Dec-2016, the company remained in the original 'AA' rating. By 31-Dec-2017, a downgrade to 'A' is recorded. Consistent with this, the transition counts show one transition from 'AA' to 'AA' (from the end of 2015 to the end of 2016), and one transition from 'AA' to 'A' (from the end of 2016 to the end of 2017). The plot shows the last rating as a dotted red line to emphasize that the last rating in the data is extrapolated indefinitely into the future. There is no extrapolation into the past; the company's history is ignored until a company rating is known for an entire transition period (31-Dec-2015 through 31-Dec-2016 in the case of 'ABC').

Compute Transition Matrix Containing NR (Not Rated) Rating

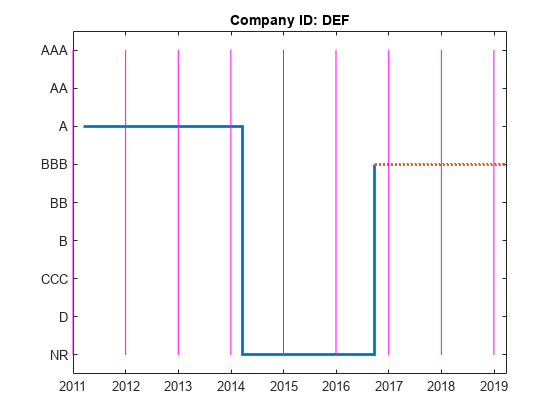

Consider a different sample data containing only a single company 'DEF'. The data contains transitions of company 'DEF' from 'A' to 'NR' rating and a subsequent transition from 'NR' to 'BBB'.

dataNR = {'DEF','17-Mar-2011','A';

'DEF','24-Mar-2014','NR';

'DEF','26-Sep-2016','BBB'};

dataNR = cell2table(dataNR,'VariableNames',{'ID','Date','Rating'});

disp(dataNR) ID Date Rating

_______ _______________ _______

{'DEF'} {'17-Mar-2011'} {'A' }

{'DEF'} {'24-Mar-2014'} {'NR' }

{'DEF'} {'26-Sep-2016'} {'BBB'}

transprob treats 'NR' as another rating. The transition matrix below shows the estimated probability of transitioning into and out of 'NR'.

StartYearNR = 2010; EndYearNR = 2018; startDateNR = datetime(StartYearNR,12,31,'Locale','en_US'); endDateNR = datetime(EndYearNR,12,31,'Locale','en_US'); CompanyID_NR = "DEF"; RatingLabelsNR = ["AAA","AA","A","BBB","BB","B","CCC","D","NR"]; [tmNR,~,itNR] = transprob(dataNR,'startDate',startDateNR,'endDate',endDateNR,'algorithm','cohort','labels',RatingLabelsNR); hDisplayTransitions(tmNR,RatingLabelsNR,"Transition Matrix")

Transition Matrix

AAA AA A BBB BB B CCC D NR

___ ___ ______ ___ ___ ___ ___ ___ ______

AAA 100 0 0 0 0 0 0 0 0

AA 0 100 0 0 0 0 0 0 0

A 0 0 66.667 0 0 0 0 0 33.333

BBB 0 0 0 100 0 0 0 0 0

BB 0 0 0 0 100 0 0 0 0

B 0 0 0 0 0 100 0 0 0

CCC 0 0 0 0 0 0 100 0 0

D 0 0 0 0 0 0 0 100 0

NR 0 0 0 50 0 0 0 0 50

Display the transition counts and corresponding visualization of the transitions.

hDisplayTransitions(itNR.totalsMat,RatingLabelsNR,strcat("Transition counts, company ID: ",CompanyID_NR))Transition counts, company ID: DEF

AAA AA A BBB BB B CCC D NR

___ __ _ ___ __ _ ___ _ __

AAA 0 0 0 0 0 0 0 0 0

AA 0 0 0 0 0 0 0 0 0

A 0 0 2 0 0 0 0 0 1

BBB 0 0 0 2 0 0 0 0 0

BB 0 0 0 0 0 0 0 0 0

B 0 0 0 0 0 0 0 0 0

CCC 0 0 0 0 0 0 0 0 0

D 0 0 0 0 0 0 0 0 0

NR 0 0 0 1 0 0 0 0 1

hPlotTransitions(CompanyID_NR,startDateNR,endDateNR,dataNR,RatingLabelsNR)

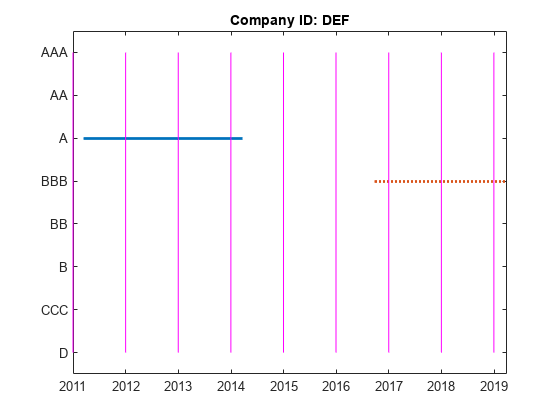

To remove the 'NR' from the transition matrix, use the 'excludeLabels' name-value input argument in transprob. The list of labels to exclude may or may not be specified in the name-value pair argument labels. For example, both RatingLabels and RatingLabelsNR generate the same output from transprob.

[tmNR,stNR,itNR] = transprob(dataNR,'startDate',startDateNR,'endDate',endDateNR,'algorithm','cohort','labels',RatingLabelsNR,'excludeLabels','NR'); hDisplayTransitions(tmNR,RatingLabels,"Transition Matrix")

Transition Matrix

AAA AA A BBB BB B CCC D

___ ___ ___ ___ ___ ___ ___ ___

AAA 100 0 0 0 0 0 0 0

AA 0 100 0 0 0 0 0 0

A 0 0 100 0 0 0 0 0

BBB 0 0 0 100 0 0 0 0

BB 0 0 0 0 100 0 0 0

B 0 0 0 0 0 100 0 0

CCC 0 0 0 0 0 0 100 0

D 0 0 0 0 0 0 0 100

Display the transition counts and corresponding visualization of the transitions.

hDisplayTransitions(itNR.totalsMat,RatingLabels,strcat("Transition counts, company ID: ",CompanyID_NR))Transition counts, company ID: DEF

AAA AA A BBB BB B CCC D

___ __ _ ___ __ _ ___ _

AAA 0 0 0 0 0 0 0 0

AA 0 0 0 0 0 0 0 0

A 0 0 2 0 0 0 0 0

BBB 0 0 0 2 0 0 0 0

BB 0 0 0 0 0 0 0 0

B 0 0 0 0 0 0 0 0

CCC 0 0 0 0 0 0 0 0

D 0 0 0 0 0 0 0 0

hPlotTransitions(CompanyID_NR,startDateNR,endDateNR,dataNR,RatingLabels)

Consistent with the previous plot, the transition counts still show two transitions from 'A' to 'A' (from the end of 2012 to the end of 2014), and two transitions from 'BBB' to 'BBB' (from the end of 2017 to the end of 2019).

However, different from the previous plot, specifying 'NR' using the 'excludeLabels' name-value input argument of transprob removes any transitions into and out of the 'NR' rating.

Local Functions

function hDisplayTransitions(TransitionsData,RatingLabels,Title) % Helper function to format transition information outputs TransitionsAsTable = array2table(TransitionsData,... 'VariableNames',RatingLabels,'RowNames',RatingLabels); fprintf('\n%s\n\n',Title) disp(TransitionsAsTable) end function hPlotTransitions(CompanyID,startDate,endDate,data,RatingLabels) % Helper function to visualize transitions between ratings Ind = string(data.ID)==CompanyID; DatesOriginal = datetime(data.Date(Ind),'Locale','en_US'); RatingsOriginal = categorical(data.Rating(Ind),flipud(RatingLabels(:)),flipud(RatingLabels(:))); stairs(DatesOriginal,RatingsOriginal,'LineWidth',2) hold on; % Indicate rating extrapolated into the future (arbitrarily select 91 % days after endDate as the last date on the plot) endDateExtrap = endDate+91; if endDateExtrap>DatesOriginal(end) DatesExtrap = [DatesOriginal(end); endDateExtrap]; RatingsExtrap = [RatingsOriginal(end); RatingsOriginal(end)]; stairs(DatesExtrap,RatingsExtrap,'LineWidth',2,'LineStyle',':') end hold off; % Add lines to indicate the snapshot dates % transprob uses 1 as the default for 'snapsPerYear', hardcoded here for simplicity % The call to cfdates generates the exact same snapshot dates that transprob uses snapsPerYear = 1; snapDates = cfdates(startDate-1,endDate,snapsPerYear)'; yLimits = ylim; for ii=1:length(snapDates) line([snapDates(ii) snapDates(ii)],yLimits,'Color','m') end title(strcat("Company ID: ",CompanyID)) end

This example shows how to visualize credit rating transitions that are used as an input to the transprob function. The example also describes how the transprob function treats rating transitions when the company data starts after the start date of the analysis, or when the end date of the analysis is after the last transition observed.

Sample Data

Set up fictitious sample data for illustration purposes.

data = {'ABC','17-Feb-2015','AA';

'ABC','6-Jul-2017','A';

'LMN','12-Aug-2014','B';

'LMN','9-Nov-2015','CCC';

'LMN','7-Sep-2016','D';

'XYZ','14-May-2013','BB';

'XYZ','21-Jun-2016','BBB'};

data = cell2table(data,'VariableNames',{'ID','Date','Rating'});

disp(data) ID Date Rating

_______ _______________ _______

{'ABC'} {'17-Feb-2015'} {'AA' }

{'ABC'} {'6-Jul-2017' } {'A' }

{'LMN'} {'12-Aug-2014'} {'B' }

{'LMN'} {'9-Nov-2015' } {'CCC'}

{'LMN'} {'7-Sep-2016' } {'D' }

{'XYZ'} {'14-May-2013'} {'BB' }

{'XYZ'} {'21-Jun-2016'} {'BBB'}

The transprob function understands that this panel-data format indicates the dates when a new rating is assigned to a given company. transprob assumes that such ratings remain unchanged, unless a subsequent row explicitly indicates a rating change. For example, for company 'ABC', transprob understands that the 'A' rating is unchanged for any date after '6-Jul-2017' (indefinitely).

Compute Transition Matrix and Transition Counts

The transprob function returns a transition probability matrix as the primary output. There are also optional outputs that contain additional information for how many transitions occurred. For more information, see transprob for information on the optional outputs for both the 'cohort' and the 'duration' methods.

For illustration purposes, this example allows you to pick the StartYear (limited to 2014 or 2015 for this example) and the EndYear (2016 or 2017). This example also uses the hDisplayTransitions helper function (see the Local Functions section) to format the transitions information for ease of reading.

StartYear =

The transition probabilities of the TransMat output indicate the probability of migrating between ratings. The probabilities are expressed in %, that is, they are multiplied by 100.

hDisplayTransitions(tm,RatingLabels,"Transition Matrix")Transition Matrix

AAA AA A BBB BB B CCC D

___ __ ___ ___ __ _ ___ ___

AAA 100 0 0 0 0 0 0 0

AA 0 50 50 0 0 0 0 0

A 0 0 100 0 0 0 0 0

BBB 0 0 0 100 0 0 0 0

BB 0 0 0 50 50 0 0 0

B 0 0 0 0 0 0 100 0

CCC 0 0 0 0 0 0 0 100

D 0 0 0 0 0 0 0 100

The transition counts are stored in the sampleTotals optional output and indicate how many transitions occurred between ratings for the entire sample (that is, all companies).

hDisplayTransitions(st.totalsMat,RatingLabels,"Transition counts, all companies")Transition counts, all companies

AAA AA A BBB BB B CCC D

___ __ _ ___ __ _ ___ _

AAA 0 0 0 0 0 0 0 0

AA 0 1 1 0 0 0 0 0

A 0 0 0 0 0 0 0 0

BBB 0 0 0 1 0 0 0 0

BB 0 0 0 1 1 0 0 0

B 0 0 0 0 0 0 1 0

CCC 0 0 0 0 0 0 0 1

D 0 0 0 0 0 0 0 1

The third output of transprob is idTotals that contains information about transitions at an ID level, company by company (in the same order that the companies appear in the input data).

Select a company to display the transition counts and a corresponding visualization of the transitions. The hPlotTransitions helper function (see the Local Functions section) shows the transitions history for a company.

CompanyID =

Transition counts, company ID: ABC

AAA AA A BBB BB B CCC D

___ __ _ ___ __ _ ___ _

AAA 0 0 0 0 0 0 0 0

AA 0 1 1 0 0 0 0 0

A 0 0 0 0 0 0 0 0

BBB 0 0 0 0 0 0 0 0

BB 0 0 0 0 0 0 0 0

B 0 0 0 0 0 0 0 0

CCC 0 0 0 0 0 0 0 0

D 0 0 0 0 0 0 0 0

hPlotTransitions(CompanyID,startDate,endDate,data,RatingLabels)

To understand how transprob handles data when the first observed date is after the start date of the analysis, or whose last observed date occurs before the end date of the analysis, consider the following example. For company 'ABC' suppose that the analysis has a start date of 31-Dec-2014 and end date of 31-Dec-2017. There are only two transitions reported for this company for that analysis time window. The first observation for 'ABC' happened on 17-Feb-2015. So the 31-Dec-2015 snapshot is the first time the company is observed. By 31-Dec-2016, the company remained in the original 'AA' rating. By 31-Dec-2017, a downgrade to 'A' is recorded. Consistent with this, the transition counts show one transition from 'AA' to 'AA' (from the end of 2015 to the end of 2016), and one transition from 'AA' to 'A' (from the end of 2016 to the end of 2017). The plot shows the last rating as a dotted red line to emphasize that the last rating in the data is extrapolated indefinitely into the future. There is no extrapolation into the past; the company's history is ignored until a company rating is known for an entire transition period (31-Dec-2015 through 31-Dec-2016 in the case of 'ABC').

Compute Transition Matrix Containing NR (Not Rated) Rating

Consider a different sample data containing only a single company 'DEF'. The data contains transitions of company 'DEF' from 'A' to 'NR' rating and a subsequent transition from 'NR' to 'BBB'.

dataNR = {'DEF','17-Mar-2011','A';

'DEF','24-Mar-2014','NR';

'DEF','26-Sep-2016','BBB'};

dataNR = cell2table(dataNR,'VariableNames',{'ID','Date','Rating'});

disp(dataNR) ID Date Rating

_______ _______________ _______

{'DEF'} {'17-Mar-2011'} {'A' }

{'DEF'} {'24-Mar-2014'} {'NR' }

{'DEF'} {'26-Sep-2016'} {'BBB'}

transprob treats 'NR' as another rating. The transition matrix below shows the estimated probability of transitioning into and out of 'NR'.

StartYearNR = 2010; EndYearNR = 2018; startDateNR = datetime(StartYearNR,12,31,'Locale','en_US'); endDateNR = datetime(EndYearNR,12,31,'Locale','en_US'); CompanyID_NR = "DEF"; RatingLabelsNR = ["AAA","AA","A","BBB","BB","B","CCC","D","NR"]; [tmNR,~,itNR] = transprob(dataNR,'startDate',startDateNR,'endDate',endDateNR,'algorithm','cohort','labels',RatingLabelsNR); hDisplayTransitions(tmNR,RatingLabelsNR,"Transition Matrix")

Transition Matrix

AAA AA A BBB BB B CCC D NR

___ ___ ______ ___ ___ ___ ___ ___ ______

AAA 100 0 0 0 0 0 0 0 0

AA 0 100 0 0 0 0 0 0 0

A 0 0 66.667 0 0 0 0 0 33.333

BBB 0 0 0 100 0 0 0 0 0

BB 0 0 0 0 100 0 0 0 0

B 0 0 0 0 0 100 0 0 0

CCC 0 0 0 0 0 0 100 0 0

D 0 0 0 0 0 0 0 100 0

NR 0 0 0 50 0 0 0 0 50

Display the transition counts and corresponding visualization of the transitions.

hDisplayTransitions(itNR.totalsMat,RatingLabelsNR,strcat("Transition counts, company ID: ",CompanyID_NR))Transition counts, company ID: DEF

AAA AA A BBB BB B CCC D NR

___ __ _ ___ __ _ ___ _ __

AAA 0 0 0 0 0 0 0 0 0

AA 0 0 0 0 0 0 0 0 0

A 0 0 2 0 0 0 0 0 1

BBB 0 0 0 2 0 0 0 0 0

BB 0 0 0 0 0 0 0 0 0

B 0 0 0 0 0 0 0 0 0

CCC 0 0 0 0 0 0 0 0 0

D 0 0 0 0 0 0 0 0 0

NR 0 0 0 1 0 0 0 0 1

hPlotTransitions(CompanyID_NR,startDateNR,endDateNR,dataNR,RatingLabelsNR)

To remove the 'NR' from the transition matrix, use the 'excludeLabels' name-value input argument in transprob. The list of labels to exclude may or may not be specified in the name-value pair argument labels. For example, both RatingLabels and RatingLabelsNR generate the same output from transprob.

[tmNR,stNR,itNR] = transprob(dataNR,'startDate',startDateNR,'endDate',endDateNR,'algorithm','cohort','labels',RatingLabelsNR,'excludeLabels','NR'); hDisplayTransitions(tmNR,RatingLabels,"Transition Matrix")

Transition Matrix

AAA AA A BBB BB B CCC D

___ ___ ___ ___ ___ ___ ___ ___

AAA 100 0 0 0 0 0 0 0

AA 0 100 0 0 0 0 0 0

A 0 0 100 0 0 0 0 0

BBB 0 0 0 100 0 0 0 0

BB 0 0 0 0 100 0 0 0

B 0 0 0 0 0 100 0 0

CCC 0 0 0 0 0 0 100 0

D 0 0 0 0 0 0 0 100

Display the transition counts and corresponding visualization of the transitions.

hDisplayTransitions(itNR.totalsMat,RatingLabels,strcat("Transition counts, company ID: ",CompanyID_NR))Transition counts, company ID: DEF

AAA AA A BBB BB B CCC D

___ __ _ ___ __ _ ___ _

AAA 0 0 0 0 0 0 0 0

AA 0 0 0 0 0 0 0 0

A 0 0 2 0 0 0 0 0

BBB 0 0 0 2 0 0 0 0

BB 0 0 0 0 0 0 0 0

B 0 0 0 0 0 0 0 0

CCC 0 0 0 0 0 0 0 0

D 0 0 0 0 0 0 0 0

hPlotTransitions(CompanyID_NR,startDateNR,endDateNR,dataNR,RatingLabels)

Consistent with the previous plot, the transition counts still show two transitions from 'A' to 'A' (from the end of 2012 to the end of 2014), and two transitions from 'BBB' to 'BBB' (from the end of 2017 to the end of 2019).

However, different from the previous plot, specifying 'NR' using the 'excludeLabels' name-value input argument of transprob removes any transitions into and out of the 'NR' rating.

Local Functions

function hDisplayTransitions(TransitionsData,RatingLabels,Title) % Helper function to format transition information outputs TransitionsAsTable = array2table(TransitionsData,... 'VariableNames',RatingLabels,'RowNames',RatingLabels); fprintf('\n%s\n\n',Title) disp(TransitionsAsTable) end function hPlotTransitions(CompanyID,startDate,endDate,data,RatingLabels) % Helper function to visualize transitions between ratings Ind = string(data.ID)==CompanyID; DatesOriginal = datetime(data.Date(Ind),'Locale','en_US'); RatingsOriginal = categorical(data.Rating(Ind),flipud(RatingLabels(:)),flipud(RatingLabels(:))); stairs(DatesOriginal,RatingsOriginal,'LineWidth',2) hold on; % Indicate rating extrapolated into the future (arbitrarily select 91 % days after endDate as the last date on the plot) endDateExtrap = endDate+91; if endDateExtrap>DatesOriginal(end) DatesExtrap = [DatesOriginal(end); endDateExtrap]; RatingsExtrap = [RatingsOriginal(end); RatingsOriginal(end)]; stairs(DatesExtrap,RatingsExtrap,'LineWidth',2,'LineStyle',':') end hold off; % Add lines to indicate the snapshot dates % transprob uses 1 as the default for 'snapsPerYear', hardcoded here for simplicity % The call to cfdates generates the exact same snapshot dates that transprob uses snapsPerYear = 1; snapDates = cfdates(startDate-1,endDate,snapsPerYear)'; yLimits = ylim; for ii=1:length(snapDates) line([snapDates(ii) snapDates(ii)],yLimits,'Color','m') end title(strcat("Company ID: ",CompanyID)) end

This example shows how to load a historical credit rating table and then use transprob to compute the exposure-based transition matrix. The sample totals and ID totals are weighted by the exposure. For more information on the computation of transition probabilities with general weights, which specializes to exposure-based probabilities, see Algorithms.

load Data_TransProb

dataExposures(1:10,:)ans=10×4 table

ID Date Rating Exposure

_____ ___________ _______ ________

10283 10-Nov-1984 {'CCC'} 8500

10283 12-May-1986 {'B' } 8500

10283 29-Jun-1988 {'CCC'} 8500

10283 12-Dec-1991 {'D' } 8500

13326 09-Feb-1985 {'A' } 7500

13326 24-Feb-1994 {'AA' } 7500

13326 10-Nov-2000 {'BBB'} 8500

14413 23-Dec-1982 {'B' } 8500

14413 20-Apr-1988 {'BB' } 8500

14413 16-Jan-1998 {'B' } 8500

The "Weight" column is the fourth column, and in this example, it is the loan's exposure on an observation date. Note that the transprob function also supports more general weights that are only required to be nonnegative and real.

Use transprob With duration Algorithm

Use transprob to estimate the exposure based transition probabilities with default settings.

[transMatExposures,sampleTotalsExposures,idTotalsExposures] = transprob(dataExposures);

Display the exposure-based transition matrix using the default settings.

transMatExposures

transMatExposures = 8×8

92.9124 6.1143 0.7937 0.1300 0.0470 0.0013 0.0001 0.0011

1.6083 93.2741 4.2951 0.6416 0.1552 0.0056 0.0005 0.0197

0.1205 3.1292 92.0483 4.0680 0.4639 0.0845 0.0034 0.0822

0.0190 0.2259 5.0466 90.1037 3.8386 0.4605 0.0819 0.2239

0.0219 0.1085 0.5943 5.9012 89.2276 3.2159 0.2776 0.6530

0.0010 0.0057 0.0654 1.0355 7.7249 85.9825 2.6259 2.5591

0.0002 0.0012 0.0131 0.3450 1.4889 4.1707 81.6593 12.3218

0 0 0 0 0 0 0 100.0000

Display the exposure-based sample totals with default settings that use the duration algorithm.

sampleTotalsExposures.totalsVec

ans = 1×8

107 ×

1.6488 2.8735 2.8788 2.5613 2.4690 1.3158 0.6614 2.1678

sampleTotalsExposures.totalsMat

ans = 8×8

0 1081500 116000 17000 7000 0 0 0

496000 0 1326500 170000 42000 0 0 5000

29000 971000 0 1280500 118500 22000 0 22500

4000 38500 1417500 0 1090000 113000 21000 53500

5500 25500 116500 1620500 0 902500 65500 153000

0 0 3000 116000 1156500 0 411000 332500

0 0 0 21500 100500 327500 0 896000

0 0 0 0 0 0 0 0

sampleTotalsExposures.algorithm

ans = 'duration'

Display the exposure-based ID totals for the second obligor (ID 13326) with default settings that use the duration algorithm.

idTotalsExposures(2).totalsVec

ans = 1×8 sparse double row vector (3 nonzeros)

1.0e+04 *

(1,2) 5.0328

(1,3) 6.7808

(1,4) 3.6445

idTotalsExposures(2).totalsMat

ans = 8×8 sparse double matrix (2 nonzeros)

(3,2) 7500

(2,4) 7500

idTotalsExposures(2).algorithm

ans = 'duration'

Use transprob With Cohort Algorithm

Use transprob to estimate the exposure-based transition probabilities with the cohort algorithm.

[transMatCohExposures,sampleTotalsCohExposures,idTotalsCohExposures] = transprob(dataExposures,algorithm="cohort");Display the exposure-based transition matrix when using the cohort algorithm.

transMatCohExposures

transMatCohExposures = 8×8

92.9468 6.1934 0.7124 0.1044 0.0430 0 0 0

1.7148 93.0587 4.4778 0.5811 0.1497 0 0 0.0178

0.1393 3.1653 91.8358 4.2990 0.4017 0.0786 0 0.0803

0.0160 0.4148 5.1063 89.7052 4.0382 0.4529 0.0521 0.2144

0.0227 0.1054 0.5992 6.3851 88.6102 3.4198 0.2707 0.5868

0 0 0.0231 0.8706 8.3320 85.5894 2.7311 2.4538

0 0 0 0.4250 1.9731 4.3181 81.1793 12.1044

0 0 0 0 0 0 0 100.0000

Display the exposure-based sample totals when using the cohort algorithm.

sampleTotalsCohExposures.totalsVec

ans = 1×8

16283500 28049500 28006500 24949500 24197000 12980000 6588500 20952000

sampleTotalsCohExposures.totalsMat

ans = 8×8

15135000 1008500 116000 17000 7000 0 0 0

481000 26102500 1256000 163000 42000 0 0 5000

39000 886500 25720000 1204000 112500 22000 0 22500

4000 103500 1274000 22381000 1007500 113000 13000 53500

5500 25500 145000 1545000 21441000 827500 65500 142000

0 0 3000 113000 1081500 11109500 354500 318500

0 0 0 28000 130000 284500 5348500 797500

0 0 0 0 0 0 0 20952000

sampleTotalsCohExposures.algorithm

ans = 'cohort'

Display the exposure-based ID totals for the second obligor (ID 13326) when using the cohort algorithm

idTotalsCohExposures(2).totalsVec

ans = 1×8 sparse double row vector (3 nonzeros)

(1,2) 45000

(1,3) 75000

(1,4) 34000

idTotalsCohExposures(2).totalsMat

ans = 8×8 sparse double matrix (5 nonzeros)

(2,2) 37500

(3,2) 7500

(3,3) 67500

(2,4) 7500

(4,4) 34000

idTotalsCohExposures(2).algorithm

ans = 'cohort'

The duration algorithm and the cohort algorithm produce similar transition matrices. In each case, the totals are weighted by the exposures. For additional details, see Algorithms.

Input Arguments

Name-Value Arguments

Output Arguments

More About

Algorithms

References

[1] Hanson, S., T. Schuermann. "Confidence Intervals for Probabilities of Default." Journal of Banking & Finance. Vol. 30(8), Elsevier, August 2006, pp. 2281–2301.

[2] Löffler, G., P. N. Posch. Credit Risk Modeling Using Excel and VBA. West Sussex, England: Wiley Finance, 2007.

[3] Schuermann, T. "Credit Migration Matrices." in E. Melnick, B. Everitt (eds.), Encyclopedia of Quantitative Risk Analysis and Assessment. Wiley, 2008.