boxcox

Box-Cox transformation

Description

[

transforms the data vector transdat,lambda] = boxcox(data)data using the Box-Cox

transformation method into transdat. It also estimates the

transformation parameter λ. For more information, see Box Cox Transformation.

transdat = boxcox(lambda,data)data using a certain specified λ for the Box-Cox

transformation. This syntax does not find the optimum λ that maximizes the LLF. For

more information, see Box Cox Transformation.

Examples

Use boxcox to transform the data series contained in a vector of data into another set of data series with relatively normal distributions.

Load the SimulatedStock.mat data file.

load SimulatedStock.matTransform the nonnormally distributed filled data series TMW_CLOSE into a normally distributed one using Box-Cox transformation.

[Xbc, lambdabc] = boxcox(TMW_CLOSE)

Xbc = 1000×1

7.8756

7.8805

7.9173

7.8557

7.8245

7.7844

7.7811

7.8029

7.8015

7.7229

7.6870

7.6825

7.7447

7.6958

7.6596

⋮

lambdabc = 0.2151

Compare the result of the TMW_CLOSE data series with a normal (Gaussian) probability distribution function and the nonnormally distributed TMW_CLOSE.

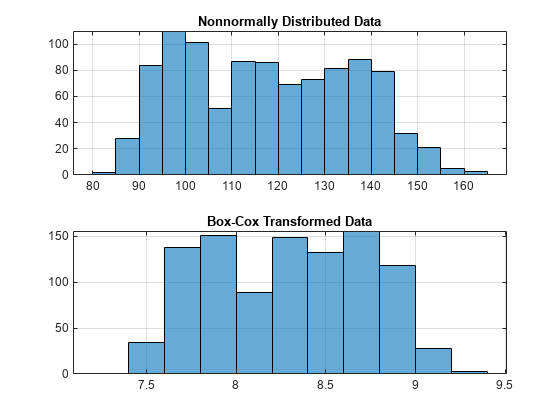

subplot(2, 1, 1); histogram(TMW_CLOSE); grid; title('Nonnormally Distributed Data'); subplot(2, 1, 2); histogram(Xbc); grid; title('Box-Cox Transformed Data');

The bar chart on the top represents the probability distribution function of the data series, TMW_CLOSE, which is the original data series. The distribution is skewed toward the left (not normally distributed). The bar chart on the bottom is less skewed to the left. If you plot a Gaussian probability distribution function (PDF) with similar mean and standard deviation, the distribution of the transformed data is close to normal (Gaussian). When you examine the contents of the resulting object Xbc, you find an identical object to the original object TMW_CLOSE but the contents are the transformed data series.