estimate

Estimate posterior distribution of Bayesian vector autoregression (VAR) model parameters

Syntax

Description

PosteriorMdl = estimate(PriorMdl,Y)PosteriorMdl that characterizes the joint posterior distributions of the coefficients Λ and innovations covariance matrix Σ. PriorMdl specifies the joint prior distribution of the parameters and the structure of the VAR model. Y is the multivariate response data. PriorMdl and PosteriorMdl might not be the same object type.

NaNs in the data indicate missing values, which estimate removes by using list-wise deletion.

PosteriorMdl = estimate(PriorMdl,Y,Name,Value)'Y0' name-value pair argument.

[ also returns an estimation summary of the posterior distribution PosteriorMdl,Summary]

= estimate(___)Summary, using any of the input argument combinations in the previous syntaxes.

Examples

Consider the 3-D VAR(4) model for the US inflation (INFL), unemployment (UNRATE), and federal funds (FEDFUNDS) rates.

For all , is a series of independent 3-D normal innovations with a mean of 0 and covariance . Assume that the joint prior distribution of the VAR model parameters is diffuse.

Load and Preprocess Data

Load the US macroeconomic data set. Compute the inflation rate. Plot all response series.

load Data_USEconModel seriesnames = ["INFL" "UNRATE" "FEDFUNDS"]; DataTimeTable.INFL = 100*[NaN; price2ret(DataTimeTable.CPIAUCSL)]; figure plot(DataTimeTable.Time,DataTimeTable{:,seriesnames}) legend(seriesnames)

Stabilize the unemployment and federal funds rates by applying the first difference to each series.

DataTimeTable.DUNRATE = [NaN; diff(DataTimeTable.UNRATE)];

DataTimeTable.DFEDFUNDS = [NaN; diff(DataTimeTable.FEDFUNDS)];

seriesnames(2:3) = "D" + seriesnames(2:3);Remove all missing values from the data.

rmDataTimeTable = rmmissing(DataTimeTable);

Create Prior Model

Create a diffuse Bayesian VAR(4) prior model for the three response series. Specify the response variable names.

numseries = numel(seriesnames);

numlags = 4;

PriorMdl = bayesvarm(numseries,numlags,'SeriesNames',seriesnames)PriorMdl =

diffusebvarm with properties:

Description: "3-Dimensional VAR(4) Model"

NumSeries: 3

P: 4

SeriesNames: ["INFL" "DUNRATE" "DFEDFUNDS"]

IncludeConstant: 1

IncludeTrend: 0

NumPredictors: 0

AR: {[3×3 double] [3×3 double] [3×3 double] [3×3 double]}

Constant: [3×1 double]

Trend: [3×0 double]

Beta: [3×0 double]

Covariance: [3×3 double]

PriorMdl is a diffusebvarm model object.

Estimate Posterior Distribution

Estimate the posterior distribution by passing the prior model and entire data series to estimate.

PosteriorMdl = estimate(PriorMdl,rmDataTimeTable{:,seriesnames})Bayesian VAR under diffuse priors

Effective Sample Size: 197

Number of equations: 3

Number of estimated Parameters: 39

| Mean Std

-------------------------------

Constant(1) | 0.1007 0.0832

Constant(2) | -0.0499 0.0450

Constant(3) | -0.4221 0.1781

AR{1}(1,1) | 0.1241 0.0762

AR{1}(2,1) | -0.0219 0.0413

AR{1}(3,1) | -0.1586 0.1632

AR{1}(1,2) | -0.4809 0.1536

AR{1}(2,2) | 0.4716 0.0831

AR{1}(3,2) | -1.4368 0.3287

AR{1}(1,3) | 0.1005 0.0390

AR{1}(2,3) | 0.0391 0.0211

AR{1}(3,3) | -0.2905 0.0835

AR{2}(1,1) | 0.3236 0.0868

AR{2}(2,1) | 0.0913 0.0469

AR{2}(3,1) | 0.3403 0.1857

AR{2}(1,2) | -0.0503 0.1647

AR{2}(2,2) | 0.2414 0.0891

AR{2}(3,2) | -0.2968 0.3526

AR{2}(1,3) | 0.0450 0.0413

AR{2}(2,3) | 0.0536 0.0223

AR{2}(3,3) | -0.3117 0.0883

AR{3}(1,1) | 0.4272 0.0860

AR{3}(2,1) | -0.0389 0.0465

AR{3}(3,1) | 0.2848 0.1841

AR{3}(1,2) | 0.2738 0.1620

AR{3}(2,2) | 0.0552 0.0876

AR{3}(3,2) | -0.7401 0.3466

AR{3}(1,3) | 0.0523 0.0428

AR{3}(2,3) | 0.0008 0.0232

AR{3}(3,3) | 0.0028 0.0917

AR{4}(1,1) | 0.0167 0.0901

AR{4}(2,1) | 0.0285 0.0488

AR{4}(3,1) | -0.0690 0.1928

AR{4}(1,2) | -0.1830 0.1520

AR{4}(2,2) | -0.1795 0.0822

AR{4}(3,2) | 0.1494 0.3253

AR{4}(1,3) | 0.0067 0.0395

AR{4}(2,3) | 0.0088 0.0214

AR{4}(3,3) | -0.1372 0.0845

Innovations Covariance Matrix

| INFL DUNRATE DFEDFUNDS

-------------------------------------------

INFL | 0.3028 -0.0217 0.1579

| (0.0321) (0.0124) (0.0499)

DUNRATE | -0.0217 0.0887 -0.1435

| (0.0124) (0.0094) (0.0283)

DFEDFUNDS | 0.1579 -0.1435 1.3872

| (0.0499) (0.0283) (0.1470)

PosteriorMdl =

conjugatebvarm with properties:

Description: "3-Dimensional VAR(4) Model"

NumSeries: 3

P: 4

SeriesNames: ["INFL" "DUNRATE" "DFEDFUNDS"]

IncludeConstant: 1

IncludeTrend: 0

NumPredictors: 0

Mu: [39×1 double]

V: [13×13 double]

Omega: [3×3 double]

DoF: 184

AR: {[3×3 double] [3×3 double] [3×3 double] [3×3 double]}

Constant: [3×1 double]

Trend: [3×0 double]

Beta: [3×0 double]

Covariance: [3×3 double]

PosteriorMdl is a conjugatebvarm model object; the posterior is analytically tractable. The command line displays the posterior means (Mean) and standard deviations (Std) of all coefficients and the innovations covariance matrix. Row AR{k}(i,j) contains the posterior estimates of , the lag k AR coefficient of response variable j in response equation i. By default, estimate uses the first four observations as a presample to initialize the model.

Display the posterior means of the AR coefficient matrices by using dot notation.

AR1 = PosteriorMdl.AR{1}AR1 = 3×3

0.1241 -0.4809 0.1005

-0.0219 0.4716 0.0391

-0.1586 -1.4368 -0.2905

AR2 = PosteriorMdl.AR{2}AR2 = 3×3

0.3236 -0.0503 0.0450

0.0913 0.2414 0.0536

0.3403 -0.2968 -0.3117

AR3 = PosteriorMdl.AR{3}AR3 = 3×3

0.4272 0.2738 0.0523

-0.0389 0.0552 0.0008

0.2848 -0.7401 0.0028

AR4 = PosteriorMdl.AR{4}AR4 = 3×3

0.0167 -0.1830 0.0067

0.0285 -0.1795 0.0088

-0.0690 0.1494 -0.1372

Consider the 3-D VAR(4) model of Estimate Posterior Distribution. In this case, fit the model to the data starting in 1970.

Load and Preprocess Data

Load the US macroeconomic data set. Compute the inflation rate, stabilize the unemployment and federal funds rates, and remove missing values.

load Data_USEconModel seriesnames = ["INFL" "UNRATE" "FEDFUNDS"]; DataTimeTable.INFL = 100*[NaN; price2ret(DataTimeTable.CPIAUCSL)]; DataTimeTable.DUNRATE = [NaN; diff(DataTimeTable.UNRATE)]; DataTimeTable.DFEDFUNDS = [NaN; diff(DataTimeTable.FEDFUNDS)]; seriesnames(2:3) = "D" + seriesnames(2:3); rmDataTimeTable = rmmissing(DataTimeTable);

Create Prior Model

Create a diffuse Bayesian VAR(4) prior model for the three response series. Specify the response variable names.

numseries = numel(seriesnames);

numlags = 4;

PriorMdl = diffusebvarm(numseries,numlags,'SeriesNames',seriesnames);Partition Time Base for Subsamples

A VAR(4) model requires p = 4 presample observations to initialize the AR component for estimation. Define index sets corresponding to the required presample and estimation samples.

idxpre = rmDataTimeTable.Time < datetime('1970','InputFormat','yyyy'); % Presample indices idxest = ~idxpre; % Estimation sample indices T = sum(idxest)

T = 157

The effective sample size is 157 observations.

Estimate Posterior Distribution

Estimate the posterior distribution. Specify only the required presample observations by using the 'Y0' name-value pair argument.

Y0 = rmDataTimeTable{find(idxpre,PriorMdl.P,'last'),seriesnames};

PosteriorMdl = estimate(PriorMdl,rmDataTimeTable{idxest,seriesnames},...

'Y0',Y0);Bayesian VAR under diffuse priors

Effective Sample Size: 157

Number of equations: 3

Number of estimated Parameters: 39

| Mean Std

-------------------------------

Constant(1) | 0.1431 0.1134

Constant(2) | -0.0132 0.0588

Constant(3) | -0.6864 0.2418

AR{1}(1,1) | 0.1314 0.0869

AR{1}(2,1) | -0.0187 0.0450

AR{1}(3,1) | -0.2009 0.1854

AR{1}(1,2) | -0.5009 0.1834

AR{1}(2,2) | 0.4881 0.0950

AR{1}(3,2) | -1.6913 0.3912

AR{1}(1,3) | 0.1089 0.0446

AR{1}(2,3) | 0.0555 0.0231

AR{1}(3,3) | -0.3588 0.0951

AR{2}(1,1) | 0.2942 0.1012

AR{2}(2,1) | 0.0786 0.0524

AR{2}(3,1) | 0.3767 0.2157

AR{2}(1,2) | 0.0208 0.2042

AR{2}(2,2) | 0.3238 0.1058

AR{2}(3,2) | -0.4530 0.4354

AR{2}(1,3) | 0.0634 0.0487

AR{2}(2,3) | 0.0747 0.0252

AR{2}(3,3) | -0.3594 0.1038

AR{3}(1,1) | 0.4503 0.1002

AR{3}(2,1) | -0.0388 0.0519

AR{3}(3,1) | 0.3580 0.2136

AR{3}(1,2) | 0.3119 0.2008

AR{3}(2,2) | 0.0966 0.1040

AR{3}(3,2) | -0.8212 0.4282

AR{3}(1,3) | 0.0659 0.0502

AR{3}(2,3) | 0.0155 0.0260

AR{3}(3,3) | -0.0269 0.1070

AR{4}(1,1) | -0.0141 0.1046

AR{4}(2,1) | 0.0105 0.0542

AR{4}(3,1) | 0.0263 0.2231

AR{4}(1,2) | -0.2274 0.1875

AR{4}(2,2) | -0.1734 0.0972

AR{4}(3,2) | 0.1328 0.3999

AR{4}(1,3) | 0.0028 0.0456

AR{4}(2,3) | 0.0094 0.0236

AR{4}(3,3) | -0.1487 0.0973

Innovations Covariance Matrix

| INFL DUNRATE DFEDFUNDS

-------------------------------------------

INFL | 0.3597 -0.0333 0.1987

| (0.0433) (0.0161) (0.0672)

DUNRATE | -0.0333 0.0966 -0.1647

| (0.0161) (0.0116) (0.0365)

DFEDFUNDS | 0.1987 -0.1647 1.6355

| (0.0672) (0.0365) (0.1969)

Consider the 3-D VAR(4) model of Estimate Posterior Distribution.

Load the US macroeconomic data set. Compute the inflation rate, stabilize the unemployment and federal funds rates, and remove missing values.

load Data_USEconModel seriesnames = ["INFL" "UNRATE" "FEDFUNDS"]; DataTimeTable.INFL = 100*[NaN; price2ret(DataTimeTable.CPIAUCSL)]; DataTimeTable.DUNRATE = [NaN; diff(DataTimeTable.UNRATE)]; DataTimeTable.DFEDFUNDS = [NaN; diff(DataTimeTable.FEDFUNDS)]; seriesnames(2:3) = "D" + seriesnames(2:3); rmDataTimeTable = rmmissing(DataTimeTable);

Create a diffuse Bayesian VAR(4) prior model for the three response series. Specify the response variable names.

numseries = numel(seriesnames);

numlags = 4;

PriorMdl = diffusebvarm(numseries,numlags,'SeriesNames',seriesnames);You can display estimation output in three ways, or turn off the display. Compare the display types.

estimate(PriorMdl,rmDataTimeTable{:,seriesnames}); % 'table', the defaultBayesian VAR under diffuse priors

Effective Sample Size: 197

Number of equations: 3

Number of estimated Parameters: 39

| Mean Std

-------------------------------

Constant(1) | 0.1007 0.0832

Constant(2) | -0.0499 0.0450

Constant(3) | -0.4221 0.1781

AR{1}(1,1) | 0.1241 0.0762

AR{1}(2,1) | -0.0219 0.0413

AR{1}(3,1) | -0.1586 0.1632

AR{1}(1,2) | -0.4809 0.1536

AR{1}(2,2) | 0.4716 0.0831

AR{1}(3,2) | -1.4368 0.3287

AR{1}(1,3) | 0.1005 0.0390

AR{1}(2,3) | 0.0391 0.0211

AR{1}(3,3) | -0.2905 0.0835

AR{2}(1,1) | 0.3236 0.0868

AR{2}(2,1) | 0.0913 0.0469

AR{2}(3,1) | 0.3403 0.1857

AR{2}(1,2) | -0.0503 0.1647

AR{2}(2,2) | 0.2414 0.0891

AR{2}(3,2) | -0.2968 0.3526

AR{2}(1,3) | 0.0450 0.0413

AR{2}(2,3) | 0.0536 0.0223

AR{2}(3,3) | -0.3117 0.0883

AR{3}(1,1) | 0.4272 0.0860

AR{3}(2,1) | -0.0389 0.0465

AR{3}(3,1) | 0.2848 0.1841

AR{3}(1,2) | 0.2738 0.1620

AR{3}(2,2) | 0.0552 0.0876

AR{3}(3,2) | -0.7401 0.3466

AR{3}(1,3) | 0.0523 0.0428

AR{3}(2,3) | 0.0008 0.0232

AR{3}(3,3) | 0.0028 0.0917

AR{4}(1,1) | 0.0167 0.0901

AR{4}(2,1) | 0.0285 0.0488

AR{4}(3,1) | -0.0690 0.1928

AR{4}(1,2) | -0.1830 0.1520

AR{4}(2,2) | -0.1795 0.0822

AR{4}(3,2) | 0.1494 0.3253

AR{4}(1,3) | 0.0067 0.0395

AR{4}(2,3) | 0.0088 0.0214

AR{4}(3,3) | -0.1372 0.0845

Innovations Covariance Matrix

| INFL DUNRATE DFEDFUNDS

-------------------------------------------

INFL | 0.3028 -0.0217 0.1579

| (0.0321) (0.0124) (0.0499)

DUNRATE | -0.0217 0.0887 -0.1435

| (0.0124) (0.0094) (0.0283)

DFEDFUNDS | 0.1579 -0.1435 1.3872

| (0.0499) (0.0283) (0.1470)

estimate(PriorMdl,rmDataTimeTable{:,seriesnames},...

'Display','equation');Bayesian VAR under diffuse priors

Effective Sample Size: 197

Number of equations: 3

Number of estimated Parameters: 39

VAR Equations

| INFL(-1) DUNRATE(-1) DFEDFUNDS(-1) INFL(-2) DUNRATE(-2) DFEDFUNDS(-2) INFL(-3) DUNRATE(-3) DFEDFUNDS(-3) INFL(-4) DUNRATE(-4) DFEDFUNDS(-4) Constant

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

INFL | 0.1241 -0.4809 0.1005 0.3236 -0.0503 0.0450 0.4272 0.2738 0.0523 0.0167 -0.1830 0.0067 0.1007

| (0.0762) (0.1536) (0.0390) (0.0868) (0.1647) (0.0413) (0.0860) (0.1620) (0.0428) (0.0901) (0.1520) (0.0395) (0.0832)

DUNRATE | -0.0219 0.4716 0.0391 0.0913 0.2414 0.0536 -0.0389 0.0552 0.0008 0.0285 -0.1795 0.0088 -0.0499

| (0.0413) (0.0831) (0.0211) (0.0469) (0.0891) (0.0223) (0.0465) (0.0876) (0.0232) (0.0488) (0.0822) (0.0214) (0.0450)

DFEDFUNDS | -0.1586 -1.4368 -0.2905 0.3403 -0.2968 -0.3117 0.2848 -0.7401 0.0028 -0.0690 0.1494 -0.1372 -0.4221

| (0.1632) (0.3287) (0.0835) (0.1857) (0.3526) (0.0883) (0.1841) (0.3466) (0.0917) (0.1928) (0.3253) (0.0845) (0.1781)

Innovations Covariance Matrix

| INFL DUNRATE DFEDFUNDS

-------------------------------------------

INFL | 0.3028 -0.0217 0.1579

| (0.0321) (0.0124) (0.0499)

DUNRATE | -0.0217 0.0887 -0.1435

| (0.0124) (0.0094) (0.0283)

DFEDFUNDS | 0.1579 -0.1435 1.3872

| (0.0499) (0.0283) (0.1470)

estimate(PriorMdl,rmDataTimeTable{:,seriesnames},...

'Display','matrix');Bayesian VAR under diffuse priors

Effective Sample Size: 197

Number of equations: 3

Number of estimated Parameters: 39

VAR Coefficient Matrix of Lag 1

| INFL(-1) DUNRATE(-1) DFEDFUNDS(-1)

--------------------------------------------------

INFL | 0.1241 -0.4809 0.1005

| (0.0762) (0.1536) (0.0390)

DUNRATE | -0.0219 0.4716 0.0391

| (0.0413) (0.0831) (0.0211)

DFEDFUNDS | -0.1586 -1.4368 -0.2905

| (0.1632) (0.3287) (0.0835)

VAR Coefficient Matrix of Lag 2

| INFL(-2) DUNRATE(-2) DFEDFUNDS(-2)

--------------------------------------------------

INFL | 0.3236 -0.0503 0.0450

| (0.0868) (0.1647) (0.0413)

DUNRATE | 0.0913 0.2414 0.0536

| (0.0469) (0.0891) (0.0223)

DFEDFUNDS | 0.3403 -0.2968 -0.3117

| (0.1857) (0.3526) (0.0883)

VAR Coefficient Matrix of Lag 3

| INFL(-3) DUNRATE(-3) DFEDFUNDS(-3)

--------------------------------------------------

INFL | 0.4272 0.2738 0.0523

| (0.0860) (0.1620) (0.0428)

DUNRATE | -0.0389 0.0552 0.0008

| (0.0465) (0.0876) (0.0232)

DFEDFUNDS | 0.2848 -0.7401 0.0028

| (0.1841) (0.3466) (0.0917)

VAR Coefficient Matrix of Lag 4

| INFL(-4) DUNRATE(-4) DFEDFUNDS(-4)

--------------------------------------------------

INFL | 0.0167 -0.1830 0.0067

| (0.0901) (0.1520) (0.0395)

DUNRATE | 0.0285 -0.1795 0.0088

| (0.0488) (0.0822) (0.0214)

DFEDFUNDS | -0.0690 0.1494 -0.1372

| (0.1928) (0.3253) (0.0845)

Constant Term

INFL | 0.1007

| (0.0832)

DUNRATE | -0.0499

| 0.0450

DFEDFUNDS | -0.4221

| 0.1781

Innovations Covariance Matrix

| INFL DUNRATE DFEDFUNDS

-------------------------------------------

INFL | 0.3028 -0.0217 0.1579

| (0.0321) (0.0124) (0.0499)

DUNRATE | -0.0217 0.0887 -0.1435

| (0.0124) (0.0094) (0.0283)

DFEDFUNDS | 0.1579 -0.1435 1.3872

| (0.0499) (0.0283) (0.1470)

Return the estimation summary, which is a structure that contains the same information regardless of display type.

[PosteriorMdl,Summary] = estimate(PriorMdl,rmDataTimeTable{:,seriesnames});Bayesian VAR under diffuse priors

Effective Sample Size: 197

Number of equations: 3

Number of estimated Parameters: 39

| Mean Std

-------------------------------

Constant(1) | 0.1007 0.0832

Constant(2) | -0.0499 0.0450

Constant(3) | -0.4221 0.1781

AR{1}(1,1) | 0.1241 0.0762

AR{1}(2,1) | -0.0219 0.0413

AR{1}(3,1) | -0.1586 0.1632

AR{1}(1,2) | -0.4809 0.1536

AR{1}(2,2) | 0.4716 0.0831

AR{1}(3,2) | -1.4368 0.3287

AR{1}(1,3) | 0.1005 0.0390

AR{1}(2,3) | 0.0391 0.0211

AR{1}(3,3) | -0.2905 0.0835

AR{2}(1,1) | 0.3236 0.0868

AR{2}(2,1) | 0.0913 0.0469

AR{2}(3,1) | 0.3403 0.1857

AR{2}(1,2) | -0.0503 0.1647

AR{2}(2,2) | 0.2414 0.0891

AR{2}(3,2) | -0.2968 0.3526

AR{2}(1,3) | 0.0450 0.0413

AR{2}(2,3) | 0.0536 0.0223

AR{2}(3,3) | -0.3117 0.0883

AR{3}(1,1) | 0.4272 0.0860

AR{3}(2,1) | -0.0389 0.0465

AR{3}(3,1) | 0.2848 0.1841

AR{3}(1,2) | 0.2738 0.1620

AR{3}(2,2) | 0.0552 0.0876

AR{3}(3,2) | -0.7401 0.3466

AR{3}(1,3) | 0.0523 0.0428

AR{3}(2,3) | 0.0008 0.0232

AR{3}(3,3) | 0.0028 0.0917

AR{4}(1,1) | 0.0167 0.0901

AR{4}(2,1) | 0.0285 0.0488

AR{4}(3,1) | -0.0690 0.1928

AR{4}(1,2) | -0.1830 0.1520

AR{4}(2,2) | -0.1795 0.0822

AR{4}(3,2) | 0.1494 0.3253

AR{4}(1,3) | 0.0067 0.0395

AR{4}(2,3) | 0.0088 0.0214

AR{4}(3,3) | -0.1372 0.0845

Innovations Covariance Matrix

| INFL DUNRATE DFEDFUNDS

-------------------------------------------

INFL | 0.3028 -0.0217 0.1579

| (0.0321) (0.0124) (0.0499)

DUNRATE | -0.0217 0.0887 -0.1435

| (0.0124) (0.0094) (0.0283)

DFEDFUNDS | 0.1579 -0.1435 1.3872

| (0.0499) (0.0283) (0.1470)

Summary

Summary = struct with fields:

Description: "3-Dimensional VAR(4) Model"

NumEstimatedParameters: 39

Table: [39×2 table]

CoeffMap: [39×1 string]

CoeffMean: [39×1 double]

CoeffStd: [39×1 double]

SigmaMean: [3×3 double]

SigmaStd: [3×3 double]

The CoeffMap field contains a list of the coefficient names. The order of the names corresponds to the order of all coefficient vector inputs and outputs. Display CoeffMap.

Summary.CoeffMap

ans = 39×1 string

"AR{1}(1,1)"

"AR{1}(1,2)"

"AR{1}(1,3)"

"AR{2}(1,1)"

"AR{2}(1,2)"

"AR{2}(1,3)"

"AR{3}(1,1)"

"AR{3}(1,2)"

"AR{3}(1,3)"

"AR{4}(1,1)"

"AR{4}(1,2)"

"AR{4}(1,3)"

"Constant(1)"

"AR{1}(2,1)"

"AR{1}(2,2)"

"AR{1}(2,3)"

"AR{2}(2,1)"

"AR{2}(2,2)"

"AR{2}(2,3)"

"AR{3}(2,1)"

"AR{3}(2,2)"

"AR{3}(2,3)"

"AR{4}(2,1)"

"AR{4}(2,2)"

"AR{4}(2,3)"

"Constant(2)"

"AR{1}(3,1)"

"AR{1}(3,2)"

"AR{1}(3,3)"

"AR{2}(3,1)"

⋮

Consider the 3-D VAR(4) model of Estimate Posterior Distribution In this example, create a normal conjugate prior model with a fixed coefficient matrix instead of a diffuse model. The model contains 39 coefficients. For coefficient sparsity in the posterior, apply the Minnesota regularization method during estimation.

Load the US macroeconomic data set. Compute the inflation rate, stabilize the unemployment and federal funds rates, and remove missing values.

load Data_USEconModel seriesnames = ["INFL" "UNRATE" "FEDFUNDS"]; DataTimeTable.INFL = 100*[NaN; price2ret(DataTimeTable.CPIAUCSL)]; DataTimeTable.DUNRATE = [NaN; diff(DataTimeTable.UNRATE)]; DataTimeTable.DFEDFUNDS = [NaN; diff(DataTimeTable.FEDFUNDS)]; seriesnames(2:3) = "D" + seriesnames(2:3); rmDataTimeTable = rmmissing(DataTimeTable);

Create a normal conjugate Bayesian VAR(4) prior model for the three response series. Specify the response variable names, and set the innovations covariance matrix

According to the Minnesota regularization method, specify the following:

Each response is an AR(1) model, on average, with lag 1 coefficient 0.75.

The prior self-lag coefficients have variance 100. This large variance setting allows the data to influence the posterior more than the prior.

The prior cross-lag coefficients have variance 0.01. This small variance setting tightens the cross-lag coefficients to zero during estimation.

Prior coefficient covariances decay with increasing lag at a rate of 10 (that is, lower lags are more important than higher lags).

numseries = numel(seriesnames); numlags = 4; Sigma = [10e-5 0 10e-4; 0 0.1 -0.2; 10e-4 -0.2 1.6]; PriorMdl = bayesvarm(numseries,numlags,'Model','normal','SeriesNames',seriesnames,... 'Center',0.75,'SelfLag',100,'CrossLag',0.01,'Decay',10,... 'Sigma',Sigma);

Estimate the posterior distribution, and display the posterior response equations.

PosteriorMdl = estimate(PriorMdl,rmDataTimeTable{:,seriesnames},'Display','equation');Bayesian VAR under normal priors and fixed Sigma

Effective Sample Size: 197

Number of equations: 3

Number of estimated Parameters: 39

VAR Equations

| INFL(-1) DUNRATE(-1) DFEDFUNDS(-1) INFL(-2) DUNRATE(-2) DFEDFUNDS(-2) INFL(-3) DUNRATE(-3) DFEDFUNDS(-3) INFL(-4) DUNRATE(-4) DFEDFUNDS(-4) Constant

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

INFL | 0.1234 -0.4373 0.1050 0.3343 -0.0342 0.0308 0.4441 0.0031 0.0090 0.0083 -0.0003 0.0003 0.0820

| (0.0014) (0.0027) (0.0007) (0.0015) (0.0021) (0.0006) (0.0015) (0.0004) (0.0003) (0.0015) (0.0001) (0.0001) (0.0014)

DUNRATE | 0.0521 0.3636 0.0125 0.0012 0.1720 0.0009 0.0000 -0.0741 -0.0000 0.0000 0.0007 -0.0000 -0.0413

| (0.0252) (0.0723) (0.0191) (0.0031) (0.0666) (0.0031) (0.0004) (0.0348) (0.0004) (0.0001) (0.0096) (0.0001) (0.0339)

DFEDFUNDS | -0.0105 -0.1394 -0.1368 0.0002 -0.0000 -0.1227 0.0000 -0.0000 0.0085 -0.0000 0.0000 -0.0041 -0.0113

| (0.0749) (0.0948) (0.0713) (0.0031) (0.0031) (0.0633) (0.0004) (0.0004) (0.0344) (0.0001) (0.0001) (0.0097) (0.1176)

Innovations Covariance Matrix

| INFL DUNRATE DFEDFUNDS

----------------------------------------

INFL | 0.0001 0 0.0010

| (0) (0) (0)

DUNRATE | 0 0.1000 -0.2000

| (0) (0) (0)

DFEDFUNDS | 0.0010 -0.2000 1.6000

| (0) (0) (0)

Compare the results to a posterior in which you specify no prior regularization.

PriorMdlNoReg = bayesvarm(numseries,numlags,'Model','normal','SeriesNames',seriesnames,... 'Sigma',Sigma); PosteriorMdlNoReg = estimate(PriorMdlNoReg,rmDataTimeTable{:,seriesnames},'Display','equation');

Bayesian VAR under normal priors and fixed Sigma

Effective Sample Size: 197

Number of equations: 3

Number of estimated Parameters: 39

VAR Equations

| INFL(-1) DUNRATE(-1) DFEDFUNDS(-1) INFL(-2) DUNRATE(-2) DFEDFUNDS(-2) INFL(-3) DUNRATE(-3) DFEDFUNDS(-3) INFL(-4) DUNRATE(-4) DFEDFUNDS(-4) Constant

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

INFL | 0.1242 -0.4794 0.1007 0.3233 -0.0502 0.0450 0.4270 0.2734 0.0523 0.0168 -0.1823 0.0068 0.1010

| (0.0014) (0.0028) (0.0007) (0.0016) (0.0030) (0.0007) (0.0016) (0.0029) (0.0008) (0.0016) (0.0027) (0.0007) (0.0015)

DUNRATE | -0.0264 0.3428 0.0089 0.0969 0.1578 0.0292 0.0042 -0.0309 -0.0114 0.0221 -0.1071 0.0072 -0.0873

| (0.0347) (0.0714) (0.0203) (0.0356) (0.0714) (0.0203) (0.0337) (0.0670) (0.0200) (0.0326) (0.0615) (0.0186) (0.0422)

DFEDFUNDS | -0.0351 -0.1248 -0.0411 0.0416 -0.0224 -0.1358 0.0014 -0.0302 0.1557 -0.0074 -0.0010 -0.0785 -0.0205

| (0.0787) (0.0949) (0.0696) (0.0631) (0.0689) (0.0663) (0.0533) (0.0567) (0.0630) (0.0470) (0.0493) (0.0608) (0.1347)

Innovations Covariance Matrix

| INFL DUNRATE DFEDFUNDS

----------------------------------------

INFL | 0.0001 0 0.0010

| (0) (0) (0)

DUNRATE | 0 0.1000 -0.2000

| (0) (0) (0)

DFEDFUNDS | 0.0010 -0.2000 1.6000

| (0) (0) (0)

The posterior estimates of the Minnesota prior have lower magnitude, in general, compared to the estimates of the default normal conjugate prior model.

Consider the 3-D VAR(4) model of Estimate Posterior Distribution In this case, assume that the coefficients and innovations covariance matrix are independent (a semiconjugate prior model).

Load the US macroeconomic data set. Compute the inflation rate, stabilize the unemployment and federal funds rates, and remove missing values.

load Data_USEconModel seriesnames = ["INFL" "UNRATE" "FEDFUNDS"]; DataTimeTable.INFL = 100*[NaN; price2ret(DataTimeTable.CPIAUCSL)]; DataTimeTable.DUNRATE = [NaN; diff(DataTimeTable.UNRATE)]; DataTimeTable.DFEDFUNDS = [NaN; diff(DataTimeTable.FEDFUNDS)]; seriesnames(2:3) = "D" + seriesnames(2:3); rmDataTimeTable = rmmissing(DataTimeTable);

Create a semiconjugate Bayesian VAR(4) prior model for the three response series. Specify the response variable names.

numseries = numel(seriesnames); numlags = 4; PriorMdl = bayesvarm(numseries,numlags,'Model','semiconjugate',... 'SeriesNames',seriesnames);

Because the joint posterior of a semiconjugate prior model is analytically intractable, estimate uses a Gibbs sampler to form the joint posterior by sampling from the tractable full conditionals.

Estimate the posterior distribution. For the Gibbs sampler, specify an effective number of draws of 20,000, a burn-in period of 5000, and a thinning factor of 10.

rng(1) % For reproducibility PosteriorMdl = estimate(PriorMdl,rmDataTimeTable{:,seriesnames},... 'Display','equation','NumDraws',20000,'Burnin',5000,'Thin',10);

Bayesian VAR under semiconjugate priors

Effective Sample Size: 197

Number of equations: 3

Number of estimated Parameters: 39

VAR Equations

| INFL(-1) DUNRATE(-1) DFEDFUNDS(-1) INFL(-2) DUNRATE(-2) DFEDFUNDS(-2) INFL(-3) DUNRATE(-3) DFEDFUNDS(-3) INFL(-4) DUNRATE(-4) DFEDFUNDS(-4) Constant

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

INFL | 0.2243 -0.0824 0.1365 0.2515 -0.0098 0.0329 0.2888 0.0311 0.0368 0.0458 -0.0206 0.0176 0.1836

| (0.0662) (0.0821) (0.0319) (0.0701) (0.0636) (0.0309) (0.0662) (0.0534) (0.0297) (0.0649) (0.0470) (0.0274) (0.0720)

DUNRATE | -0.0262 0.3666 0.0148 0.0929 0.1637 0.0336 0.0016 -0.0147 -0.0089 0.0222 -0.1133 0.0082 -0.0808

| (0.0342) (0.0728) (0.0197) (0.0354) (0.0713) (0.0198) (0.0334) (0.0671) (0.0194) (0.0320) (0.0606) (0.0179) (0.0407)

DFEDFUNDS | -0.0251 -0.1285 -0.0527 0.0379 -0.0256 -0.1452 -0.0040 -0.0360 0.1516 -0.0090 0.0008 -0.0823 -0.0193

| (0.0785) (0.0962) (0.0673) (0.0630) (0.0688) (0.0643) (0.0531) (0.0567) (0.0610) (0.0467) (0.0492) (0.0586) (0.1302)

Innovations Covariance Matrix

| INFL DUNRATE DFEDFUNDS

-------------------------------------------

INFL | 0.2984 -0.0219 0.1754

| (0.0305) (0.0121) (0.0499)

DUNRATE | -0.0219 0.0890 -0.1496

| (0.0121) (0.0092) (0.0292)

DFEDFUNDS | 0.1754 -0.1496 1.4754

| (0.0499) (0.0292) (0.1506)

PosteriorMdl is an empiricalbvarm model represented by draws from the full conditionals. After removing the first burn-in period draws and thinning the remaining draws by keeping every 10th draw, estimate stores the draws in the CoeffDraws and SigmaDraws properties.

Consider the 2-D VARX(1) model for the US real GDP (RGDP) and investment (GCE) rates that treats the personal consumption (PCEC) rate as exogenous:

For all , is a series of independent 2-D normal innovations with a mean of 0 and covariance . Assume the following prior distributions:

, where M is a 4-by-2 matrix of means and is the 4-by-4 among-coefficient scale matrix. Equivalently, .

, where Ω is the 2-by-2 scale matrix and is the degrees of freedom.

Load the US macroeconomic data set. Compute the real GDP, investment, and personal consumption rate series. Remove all missing values from the resulting series.

load Data_USEconModel DataTimeTable.RGDP = DataTimeTable.GDP./DataTimeTable.GDPDEF; seriesnames = ["PCEC"; "RGDP"; "GCE"]; rates = varfun(@price2ret,DataTimeTable,'InputVariables',seriesnames); rates = rmmissing(rates); rates.Properties.VariableNames = seriesnames;

Create a conjugate prior model for the 2-D VARX(1) model parameters.

numseries = 2; numlags = 1; numpredictors = 1; PriorMdl = conjugatebvarm(numseries,numlags,'NumPredictors',numpredictors,... 'SeriesNames',seriesnames(2:end));

Estimate the posterior distribution. Specify the exogenous predictor data.

PosteriorMdl = estimate(PriorMdl,rates{:,2:end},...

'X',rates{:,1},'Display','equation');Bayesian VAR under conjugate priors

Effective Sample Size: 247

Number of equations: 2

Number of estimated Parameters: 8

VAR Equations

| RGDP(-1) GCE(-1) Constant X1

-----------------------------------------------

RGDP | 0.0083 -0.0027 0.0078 0.0105

| (0.0625) (0.0606) (0.0043) (0.0625)

GCE | 0.0059 0.0477 0.0166 0.0058

| (0.0644) (0.0624) (0.0044) (0.0645)

Innovations Covariance Matrix

| RGDP GCE

---------------------------

RGDP | 0.0040 0.0000

| (0.0004) (0.0003)

GCE | 0.0000 0.0043

| (0.0003) (0.0004)

By default, estimate uses the first p = 1 observations in the specified response data as a presample, and it removes the corresponding observations in the predictor data from the sample.

The posterior means (and standard deviations) of the regression coefficients appear below the X1 column of the estimation summary table.

Input Arguments

Name-Value Arguments

Output Arguments

More About

Tips

Monte Carlo simulation is subject to variation. If

estimateuses Monte Carlo simulation, then estimates and inferences might vary when you callestimatemultiple times under seemingly equivalent conditions. To reproduce estimation results, set a random number seed by usingrngbefore callingestimate.

Algorithms

Whenever the prior distribution

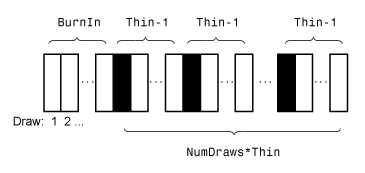

PriorMdland the data likelihood yield an analytically tractable posterior distribution,estimateevaluates the closed-form solutions to Bayes estimators. Otherwise,estimateuses the Gibbs sampler to estimate the posterior.This figure illustrates how

estimatereduces the Monte Carlo sample using the values ofNumDraws,Thin, andBurnIn. Rectangles represent successive draws from the distribution.estimateremoves the white rectangles from the Monte Carlo sample. The remainingNumDrawsblack rectangles compose the Monte Carlo sample.

Version History

Introduced in R2020a