Compare Concentration Indices for Random Portfolios

This example shows how to simulate random portfolios with different distributions and compare their concentration indices. For illustration purposes, a lognormal and Weibull distribution are used. The distribution parameters are chosen arbitrarily to get a similar range of values for both random portfolios.

Generate random portfolios with different distributions.

rng('default'); % for reproducibility PLgn = lognrnd(1,1,1,300); PWbl = wblrnd(2,0.5,1,300);

Display largest simulated loan value.

fprintf('\nLargest loan Lognormal: %g\n',max(PLgn));Largest loan Lognormal: 97.3582

fprintf('Largest loan Weibull: %g\n',max(PWbl));Largest loan Weibull: 91.5866

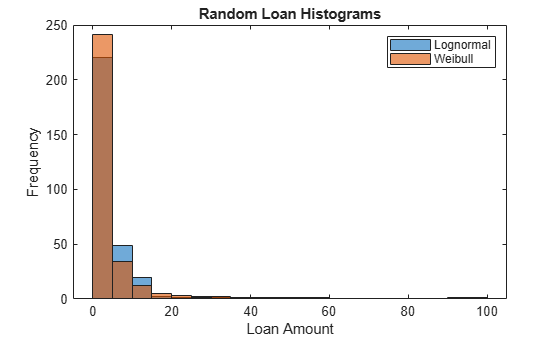

Plot the portfolio histograms.

figure; histogram(PLgn,0:5:100) hold on histogram(PWbl,0:5:100) hold off title('Random Loan Histograms') xlabel('Loan Amount') ylabel('Frequency') legend('Lognormal','Weibull')

Compute and display the concentration measures.

ciLgn = concentrationIndices(PLgn,'ID','Lognormal'); ciWbl = concentrationIndices(PWbl,'ID','Weibull'); disp([ciLgn;ciWbl])

ID CR Deciles Gini HH HK HT TE

___________ ________ _____________________________________________________________________________________________________________________________________________ _______ ________ _________ _________ _______

"Lognormal" 0.066363 0 0.0092101 0.027425 0.053898 0.093295 0.14165 0.20292 0.28269 0.39183 0.55181 1 0.5686 0.013298 0.0045765 0.0077267 0.66735

"Weibull" 0.090152 0 0.00036887 0.0031072 0.010104 0.021833 0.04367 0.081361 0.13838 0.24197 0.43317 1 0.72876 0.020197 0.0062594 0.012289 1.0944

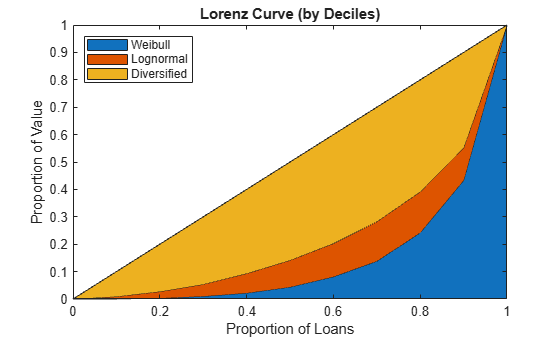

ProportionLoans = 0:0.1:1; figure; area(ProportionLoans',[ciWbl.Deciles; ciLgn.Deciles-ciWbl.Deciles; ProportionLoans-ciLgn.Deciles]') axis([0 1 0 1]) legend('Weibull','Lognormal','Diversified','Location','NorthWest') title('Lorenz Curve (by Deciles)') xlabel('Proportion of Loans') ylabel('Proportion of Value')