mvtcdf

Multivariate t cumulative distribution function

Syntax

y = mvtcdf(X,C,DF)

y = mvtcdf(xl,xu,C,DF)

[y,err] = mvtcdf(...)

[...] = mvntdf(...,options)

Description

y = mvtcdf(X,C,DF) returns

the cumulative probability of the multivariate t distribution

with correlation parameters C and degrees of freedom DF,

evaluated at each row of X. Rows of the n-by-d matrix X correspond

to observations or points, and columns correspond to variables or

coordinates. y is an n-by-1 vector.

C is a symmetric, positive definite, d-by-d matrix,

typically a correlation matrix. If its diagonal elements are not 1, mvtcdf scales C to

correlation form. mvtcdf does not rescale X. DF is

a scalar, or a vector with n elements.

The multivariate t cumulative probability

at X is defined as the probability that a random

vector T, distributed as multivariate t,

will fall within the semi-infinite rectangle with upper limits defined

by X, i.e., Pr{T(1)≤X(1),T(2)≤X(2),...T(d)≤X(d)}.

y = mvtcdf(xl,xu,C,DF) returns

the multivariate t cumulative probability evaluated

over the rectangle with lower and upper limits defined by xl and xu,

respectively.

[y,err] = mvtcdf(...) returns

an estimate of the error in y. For bivariate and

trivariate distributions, mvtcdf uses adaptive

quadrature on a transformation of the t density,

based on methods developed by Genz, as described in the references.

The default absolute error tolerance for these cases is 1e-8.

For four or more dimensions, mvtcdf uses a quasi-Monte

Carlo integration algorithm based on methods developed by Genz and

Bretz, as described in the references. The default absolute error

tolerance for these cases is 1e-4.

[...] = mvntdf(...,options) specifies

control parameters for the numerical integration used to compute y.

This argument can be created by a call to statset.

Choices of statset parameters are:

'TolFun'— Maximum absolute error tolerance. Default is1e-8when d < 4, or1e-4when d ≥ 4.'MaxFunEvals'— Maximum number of integrand evaluations allowed when d ≥ 4. Default is1e7.'MaxFunEvals'is ignored when d < 4.'Display'— Level of display output. Choices are'off'(the default),'iter', and'final'.'Display'is ignored when d < 4.

Examples

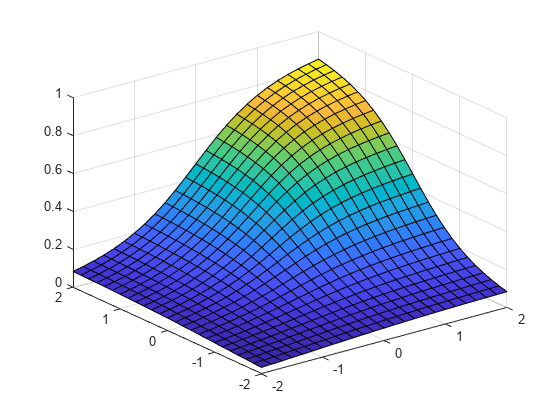

Compute the Multivariate t Distribution cdf

Compute the cdf of a multivariate t distribution with correlation parameters C = [1 .4; .4 1] and 2 degrees of freedom.

C = [1 .4; .4 1]; df = 2; [X1,X2] = meshgrid(linspace(-2,2,25)',linspace(-2,2,25)'); X = [X1(:) X2(:)]; p = mvtcdf(X,C,df);

Plot the cdf.

figure; surf(X1,X2,reshape(p,25,25));

References

[1] Genz, A. “Numerical Computation of Rectangular Bivariate and Trivariate Normal and t Probabilities.” Statistics and Computing. Vol. 14, No. 3, 2004, pp. 251–260.

[2] Genz, A., and F. Bretz. “Numerical Computation of Multivariate t Probabilities with Application to Power Calculation of Multiple Contrasts.” Journal of Statistical Computation and Simulation. Vol. 63, 1999, pp. 361–378.

[3] Genz, A., and F. Bretz. “Comparison of Methods for the Computation of Multivariate t Probabilities.” Journal of Computational and Graphical Statistics. Vol. 11, No. 4, 2002, pp. 950–971.

Version History

Introduced in R2006a

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)